-

-

2019 Business Results

Greetings and Summary

Greetings. I am Peter Kwon, the Head of IR at KBFG. We will now begin the 2019 business results presentation.

I would like to express my deepest gratitude to everyone for participating in our call. We have here with us our group CFO and Deputy President, Kim Ki-Hwan, as well as other members from our group management. We will first hear the 2019 major financial highlights from our CFO and Deputy President, Kim Ki-Hwan, and then have a Q&A session. I would like to invite our CFO and Deputy President to elaborate on our 2019 business results highlights.

Yes. Good afternoon. This is Ki-Hwan Kim, Deputy President and CFO of KB Financial Group. I'd like to extend my sincere appreciation to everyone for joining us today at KBFG's earnings release for full year 2019.

Before beginning with our presentation of financial results, let me briefly take you through our key management highlights for 2019. In 2019, as the U.S.-China trade conflict became protracted, we saw a significant escalation of concerns over a global economic slowdown and the Korean economy entering a low-rate, low-growth trajectory going forward. For the banking business in particular, there have been consistent concerns of a deterioration in profitability due to diminished goal for further growth, together with a squeeze in the loan-to-deposit margin. In spite of this negative business environment, however, KBFG Group placed utmost priority on financial soundness and profit-driven operations and as a result, we were able to achieve qualitative growth centered on a high-quality loan book, defend our net interest margin, and improve noninterest income, ultimately reaching KRW3.3 trillion in net profit and recurring ROE of 9.51%, which display KB’s strong underlying fundamentals. Moreover, as part of KB Financial Group's efforts toward enhancing shareholder value, we were the first banking financial holding group in Korea to retire roughly 2.3 million treasury shares last December, which was assessed as a firm step toward more advanced shareholder return policies.

For your reference, our Board of Directors resolved on a dividend payout of 26% for 2019 at today's BOD meeting, which is 1.2 percentage points higher than last year, as part of progressive dividend policies. Also, this year's dividend per share is KRW 2,210, which is 15.1% higher than last year as a result of improved financials and additional buyback of treasury shares. Going forward, KB Financial Group will continue to enforce diverse shareholder return measures on the strength of our robust capital position.

Over the past year, in 2019, KBFG has been working to speed up our globalization initiatives as well. One example everyone is aware is our December acquisition of a 70% stake in Cambodia's largest micro finance institution, PRASAC. We believe that the acquisition will help us overcome limitations of organic growth on the global front, helping the platform for further scale-up of our global business. In addition, last November, we were the first in the financial industry to launch Liiv M, our MVNO or mobile virtual network operator services, as we step up efforts to acquire further growth drivers for the future. Liiv M is all about delivering an altogether new form of convenient financial services, powered by digital innovation using telecommunications as a medium for enhancing KBFG's competitiveness.

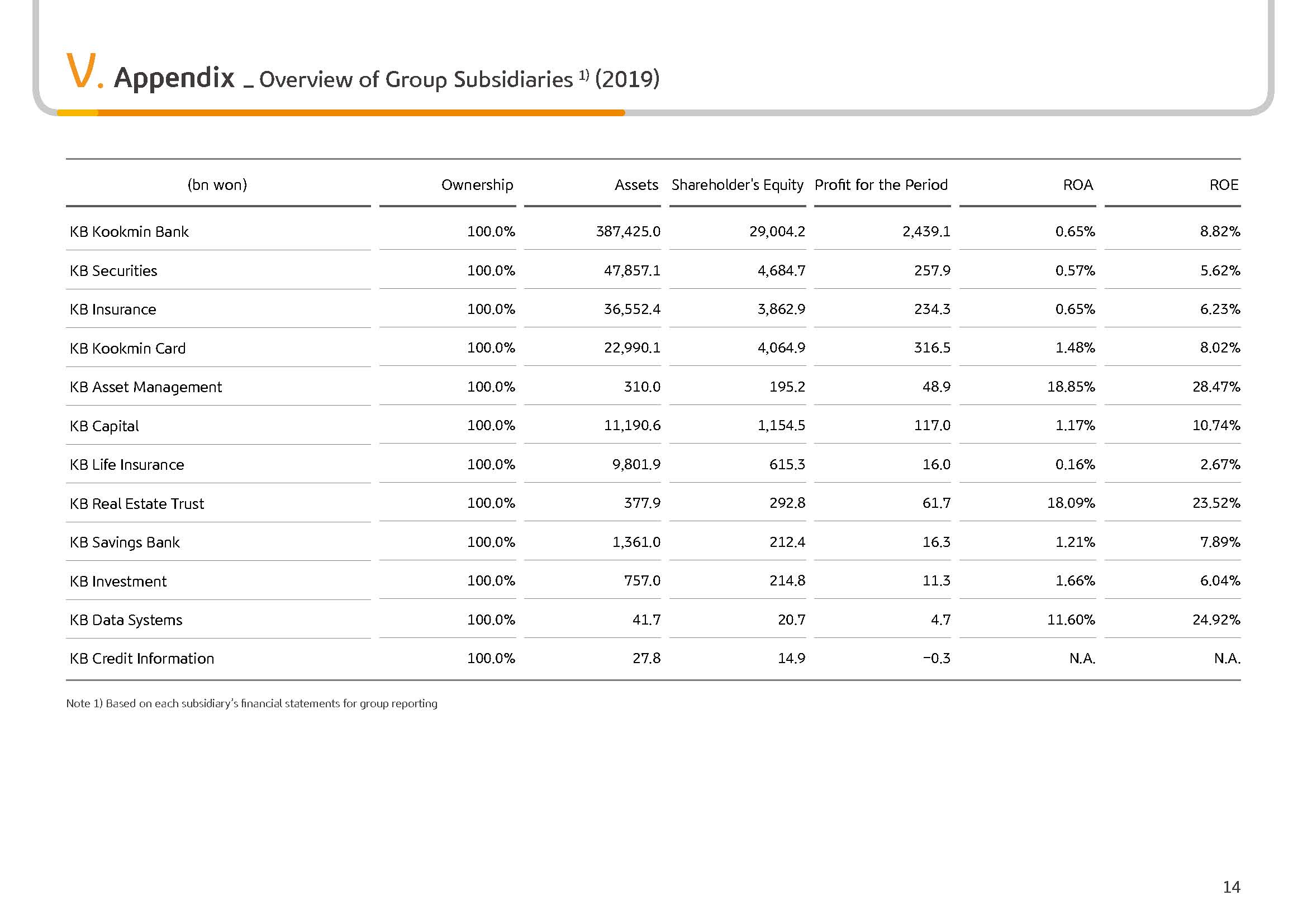

Lastly, over the last year, each of our respective subsidiaries has set out to strengthen the competitiveness of their core businesses. KB Securities, for example, started ramping up its promissory note issuance business starting May last year, expanding its earnings base as a mega IB. KB Card, meanwhile, has focused on enforcing stricter cost efficiency despite being weighed by emergency cuts, growing its market share with a focus on high-quality customers, making stable profitability as a result.

This year in 2020, we intend to continue to focus on further strengthening of our competitiveness as a group. The competitiveness of our core businesses to solidify the basis for sustainable growth, driven by bold, customer-centric innovation, so that we can again springboard into a leading financial group leading the group. I will explain the direction of our overall management strategies in the later slides.

(2p) 2019 Financial Highlights-Overview

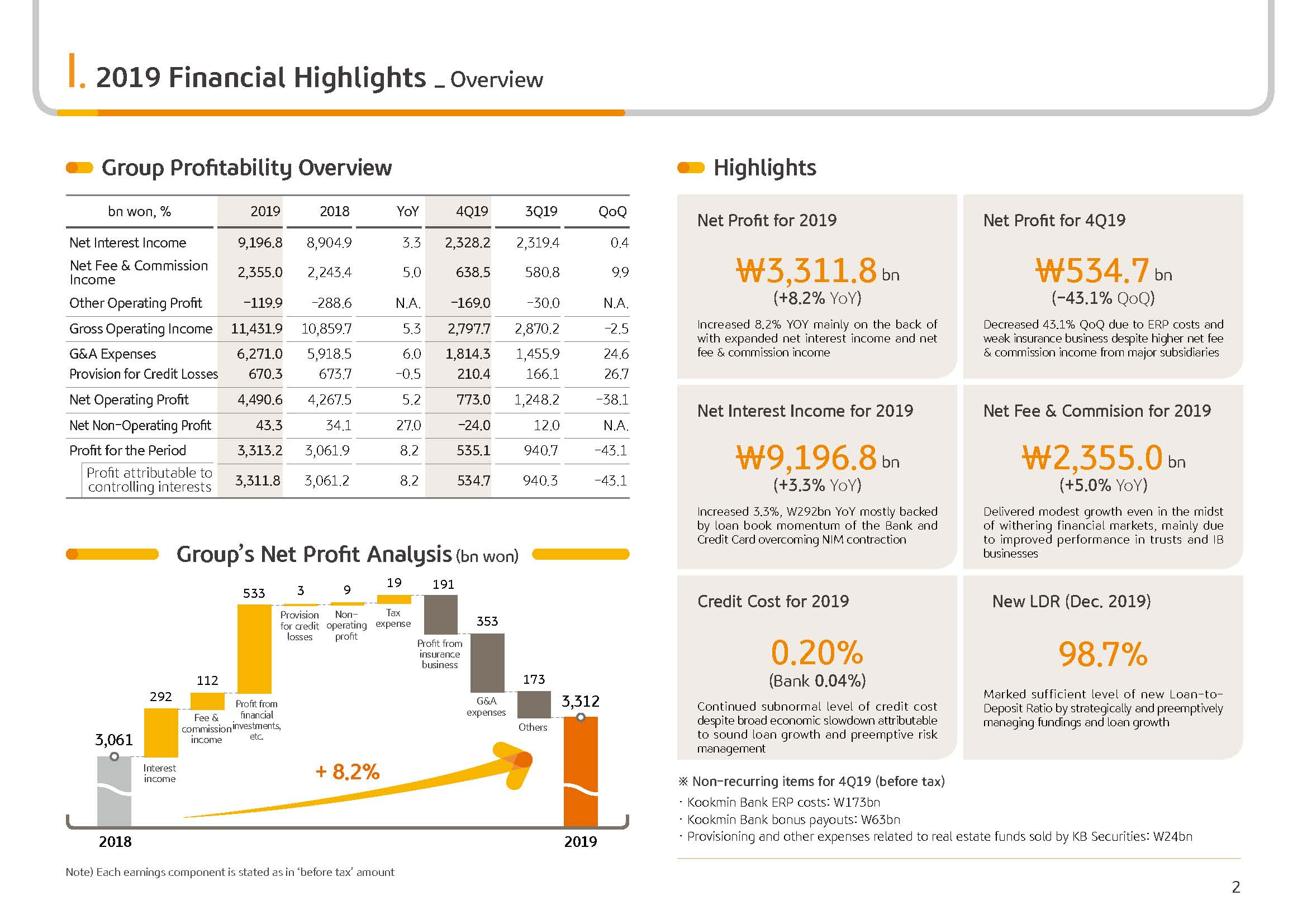

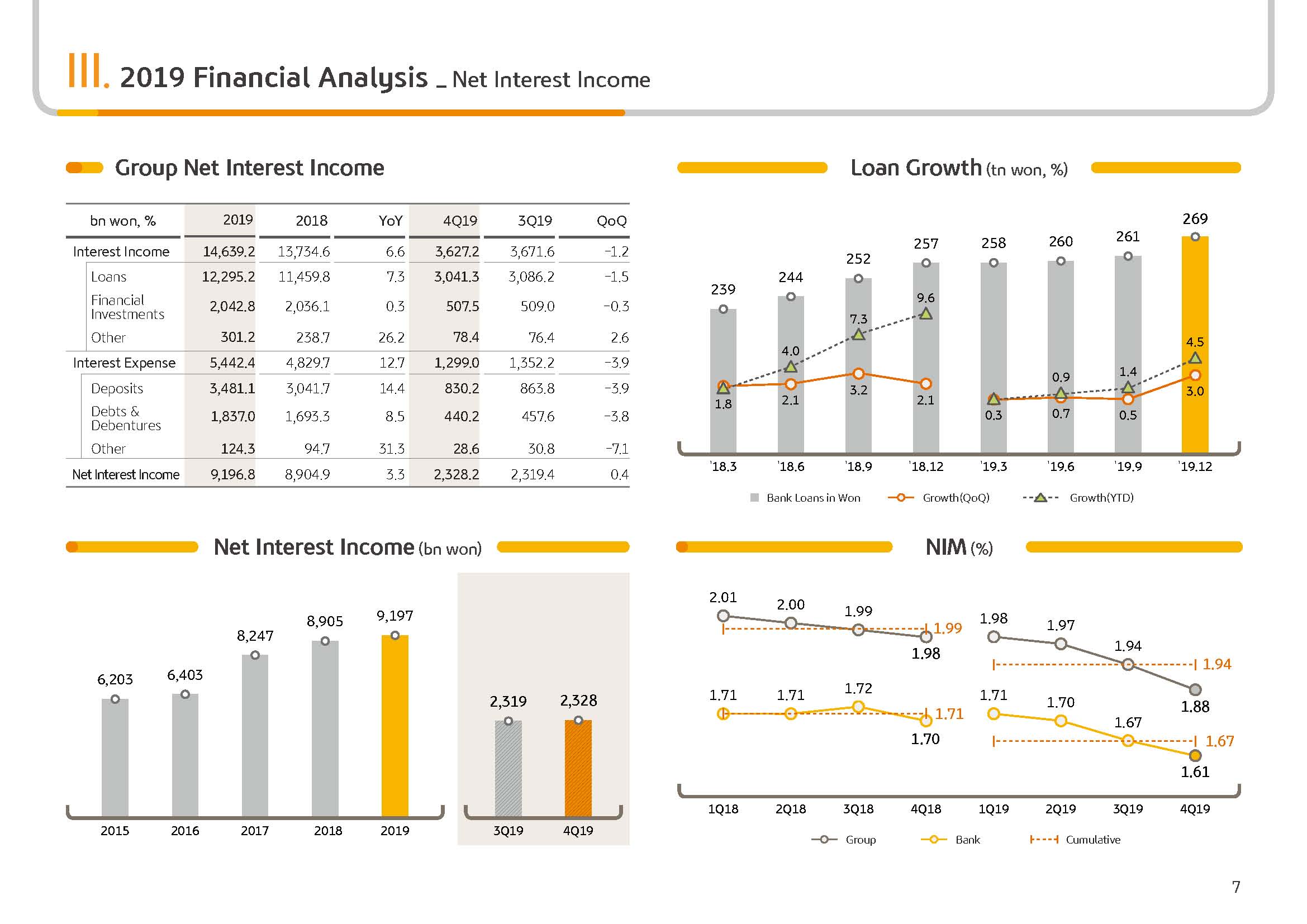

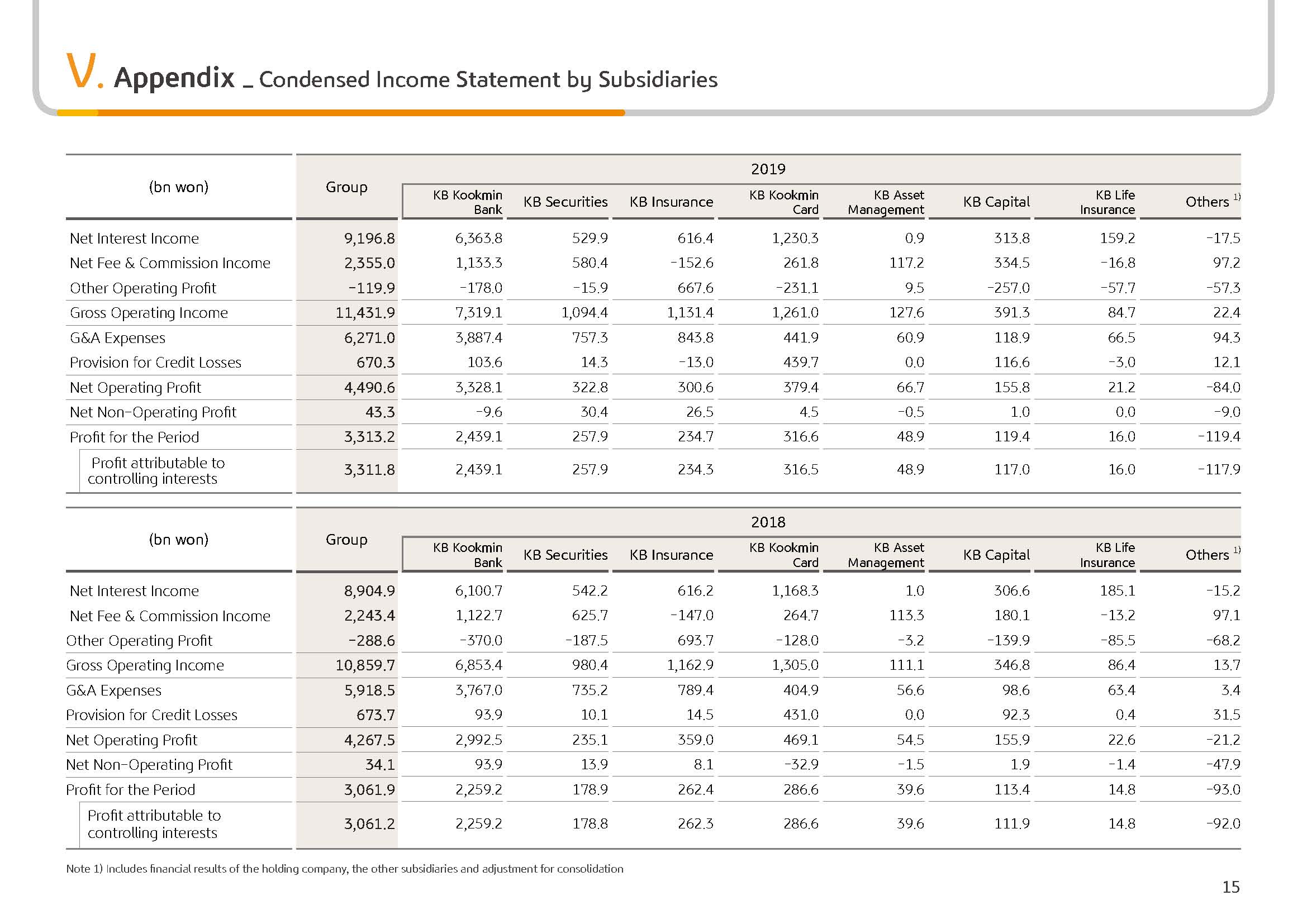

Now let's look at our results in greater detail by business area. On a group-wide basis, net interest income was KRW9,196.8 billion, growing by 3.3% year-on-year or KRW291.9 billion, driven by loan growth in banking and cards. In the fourth quarter alone, net interest income growth was rather limited to 0.4% due to a drop in loan-to-deposit margin from falling market interest rates and also from origination of conversion loans, which led to an accelerated amortization of LOC.

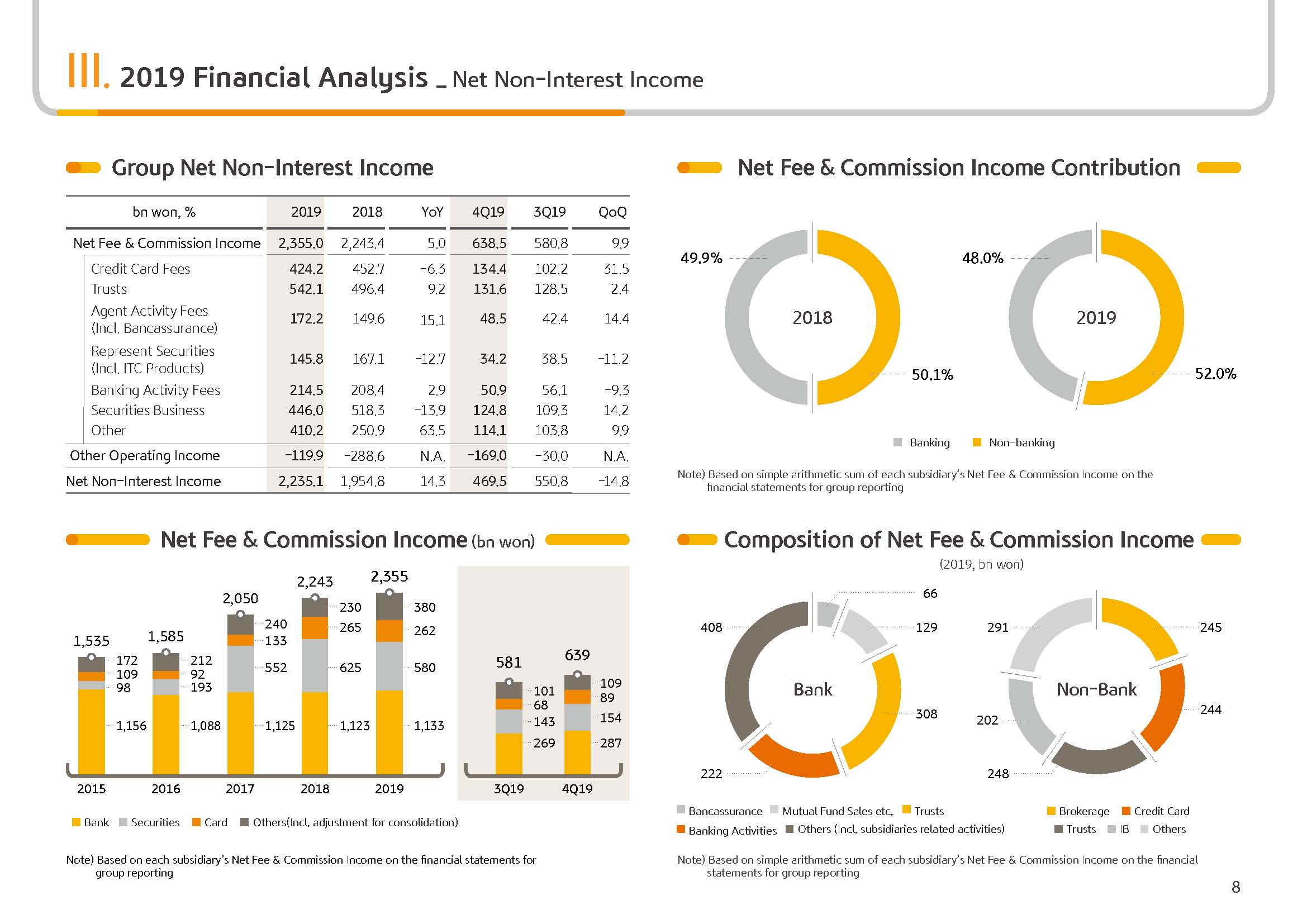

Next is our net fees and commission income. Full year 2019 net fees and commission income was KRW2,355 billion, a 5% increase year-on-year. This was possible due to a steady increase in Kookmin Bank's trust income and also KBFG's IB commissions, which helped offset the effect of a significant decline in securities custody fee income. Fourth quarter net fees and commission income was KRW638.5 billion, a 9.9% increase Q-on-Q, thanks to an increase in end-of-the-year credit card sales, an increase in credit card fee income and also improved IB performance from our banking and securities arms.

Next, on to our other operating income. Although we recorded an operating loss of KRW119.9 billion in 2019, it was nevertheless an improvement of KRW168.7 billion compared to the previous year. This was mostly because despite a slight decline in insurance earnings from a deterioration in low rates, nonetheless, we saw an increase in valuation gain on bond holding from falling market rates and a significant improvement in S&T investment earnings, which performed poorly last year. Meanwhile, we recorded other operating loss of KRW169 billion in the fourth quarter, which is a slight widening of loss from the previous quarter. This is due to a continued slowdown in insurance performance, compounded by an upturn in market rates in the fourth quarter after its bottoming out in Q3, which led to the increase in valuation loss on bond holdings.

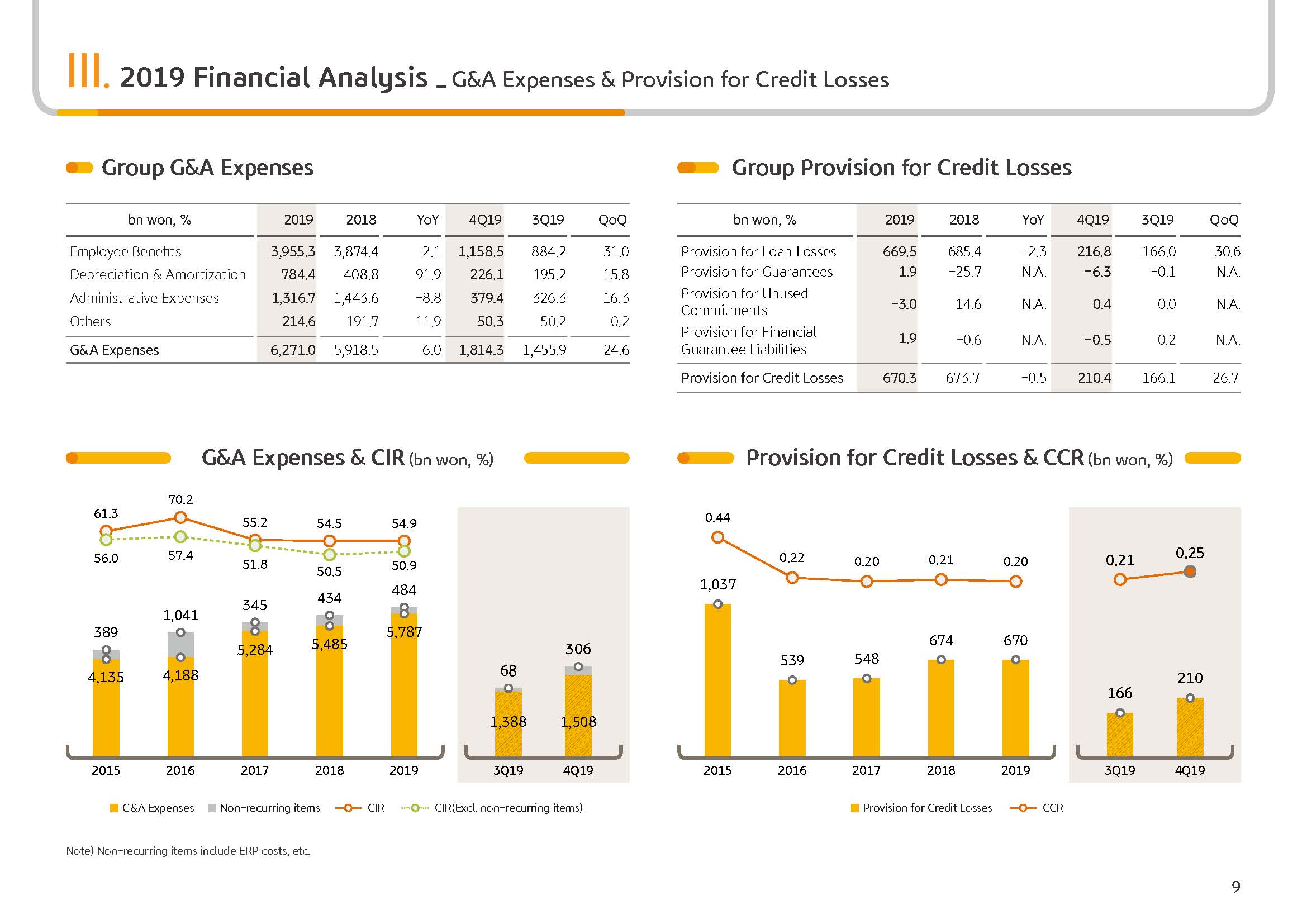

Next, on to G&A expenses. In 2019, G&A totaled KRW 6,271 billion, which is a 6% increase year-on-year. The rise in G&A appears slightly high, but this is mostly due to about KRW240 billion in voluntary ERP expenses incurred from the bank and insurance side as well as KRW180 billion in additional expenses from our group-wide digitization program. When taking out these one-off items, however, full year G&A expenses saw a moderate increase of 4.4% year-on-year. G&A in the fourth quarter was KRW1,814.3 billion, representing an increase, again, due to roughly KRW173 billion in ERP-related expenses from the bank and also a seasonal increase in advertisement and promotion expenses.

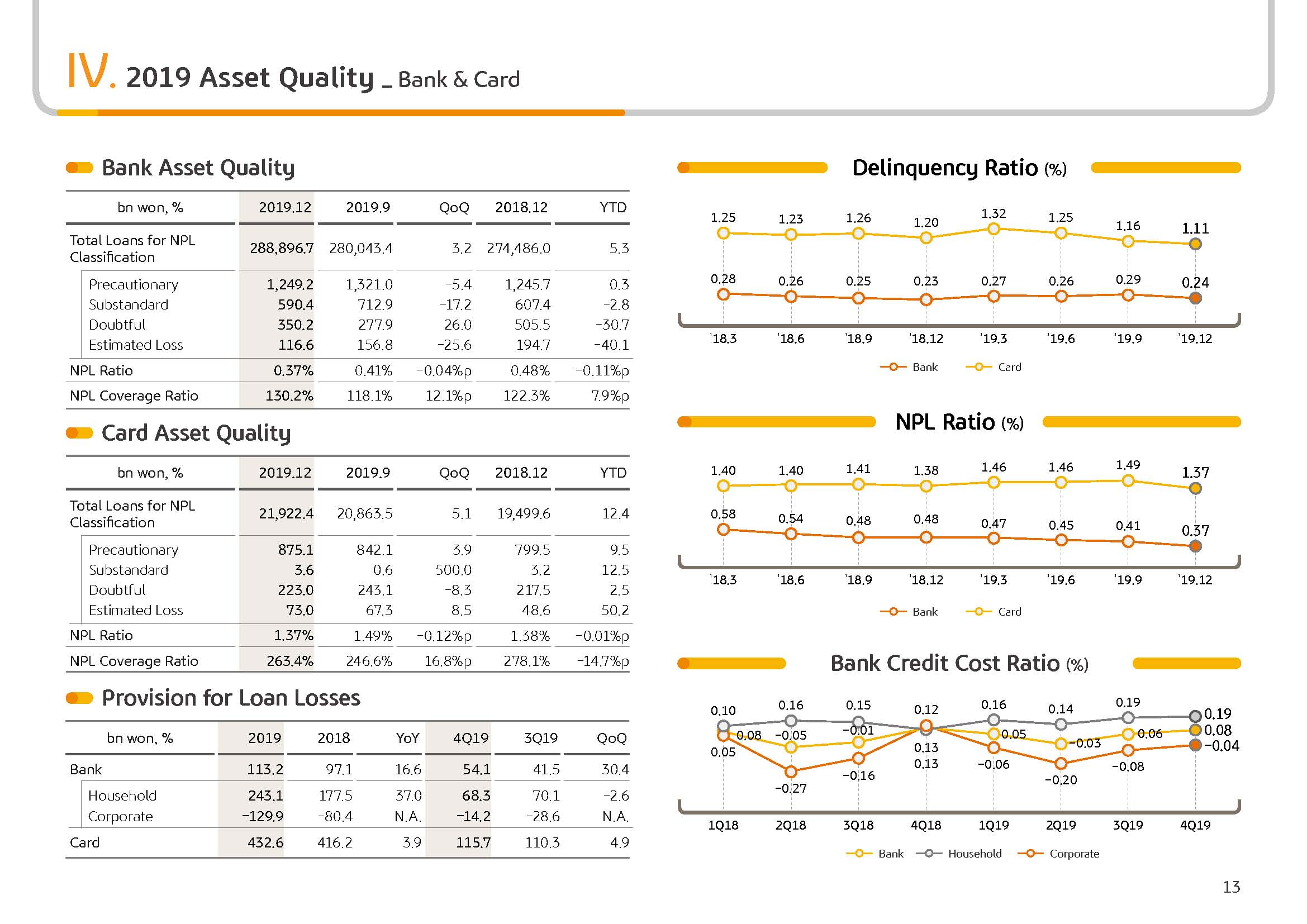

Next, moving on to PCL, which is provisions for credit loss. For full year 2019, PCL was KRW670.3 billion, which is a slight decrease year-on-year due to qualitative growth in high-quality loan assets and a reversal in loan loss provisions. As a group, our credit cost maintained subnormal levels at 20 bp. And even on a normalized basis, after taking out the one-off effect from the reversal, credit cost is 25 bp. Meanwhile, PCL in Q4 increased slightly to KRW210.4 billion on Q-on-Q basis due to the effect of last quarter’s reversal related to KCI. But apart from this one-off factor, PCL was otherwise quite moderate.

And next, we recorded non-operating loss of KRW24 billion in the fourth quarter 2019, mostly due to seasonal end-of-the-year factors, including increase in social contribution donations and also partly due to recognition of provisions related to Australian real estate funds distributed by KB Securities.

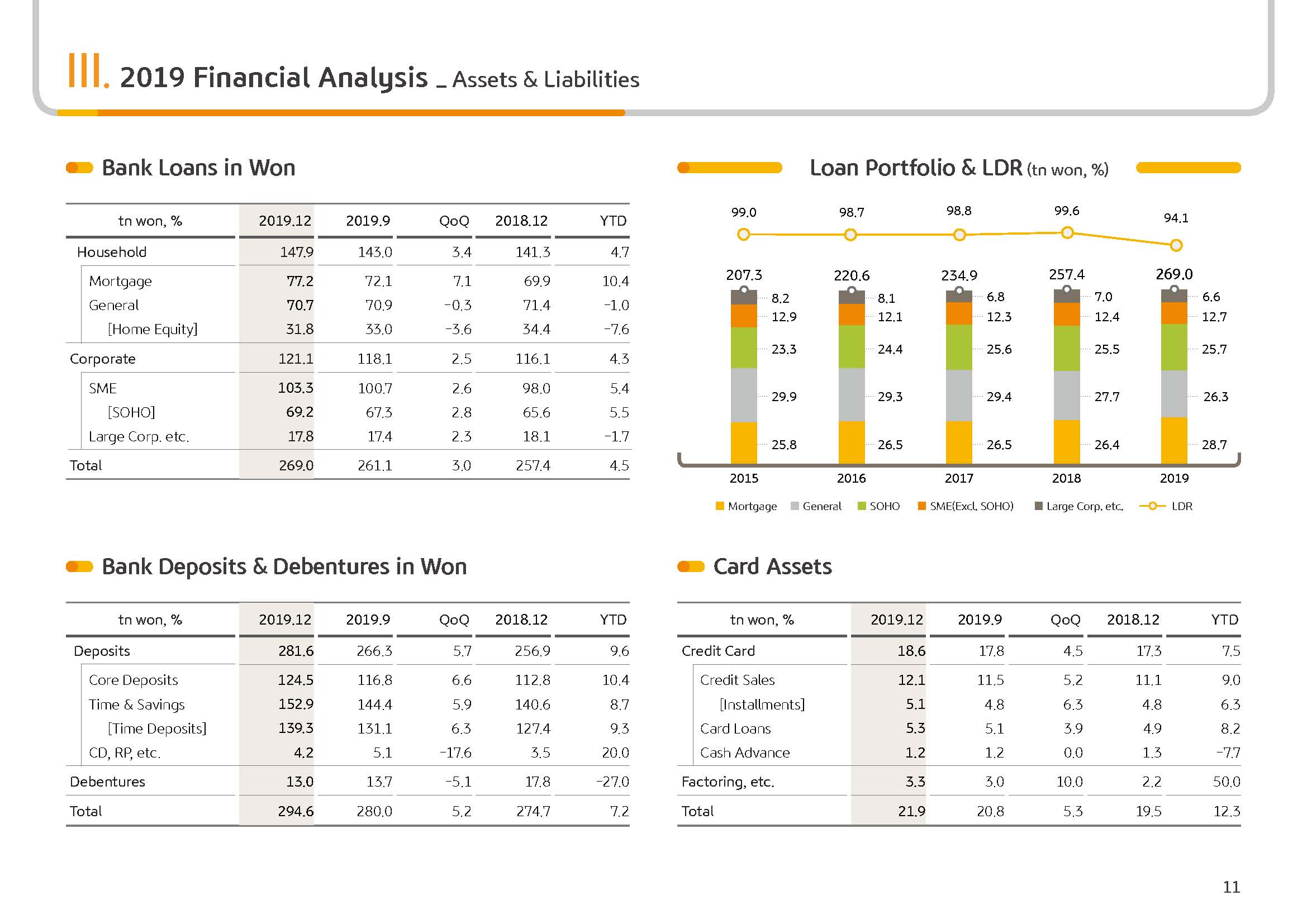

Lastly, let me briefly explain about the new loan-to-deposit ratio scheme that will go into effect this year. As of December end, the new loan-to-deposit ratio for Kookmin Bank stands at 98.7%. Kookmin Bank responded both preemptively and strategically ahead of implementation of the new regulations, making active use of covered bonds while focusing on securing more low-cost core demand deposits and high-quality corporate loans, as a result, has been steeply maintaining loan deposit rates well within the new regulatory thresholds.

(3p) 2019 Financial Highlights-Key Financial Indicators

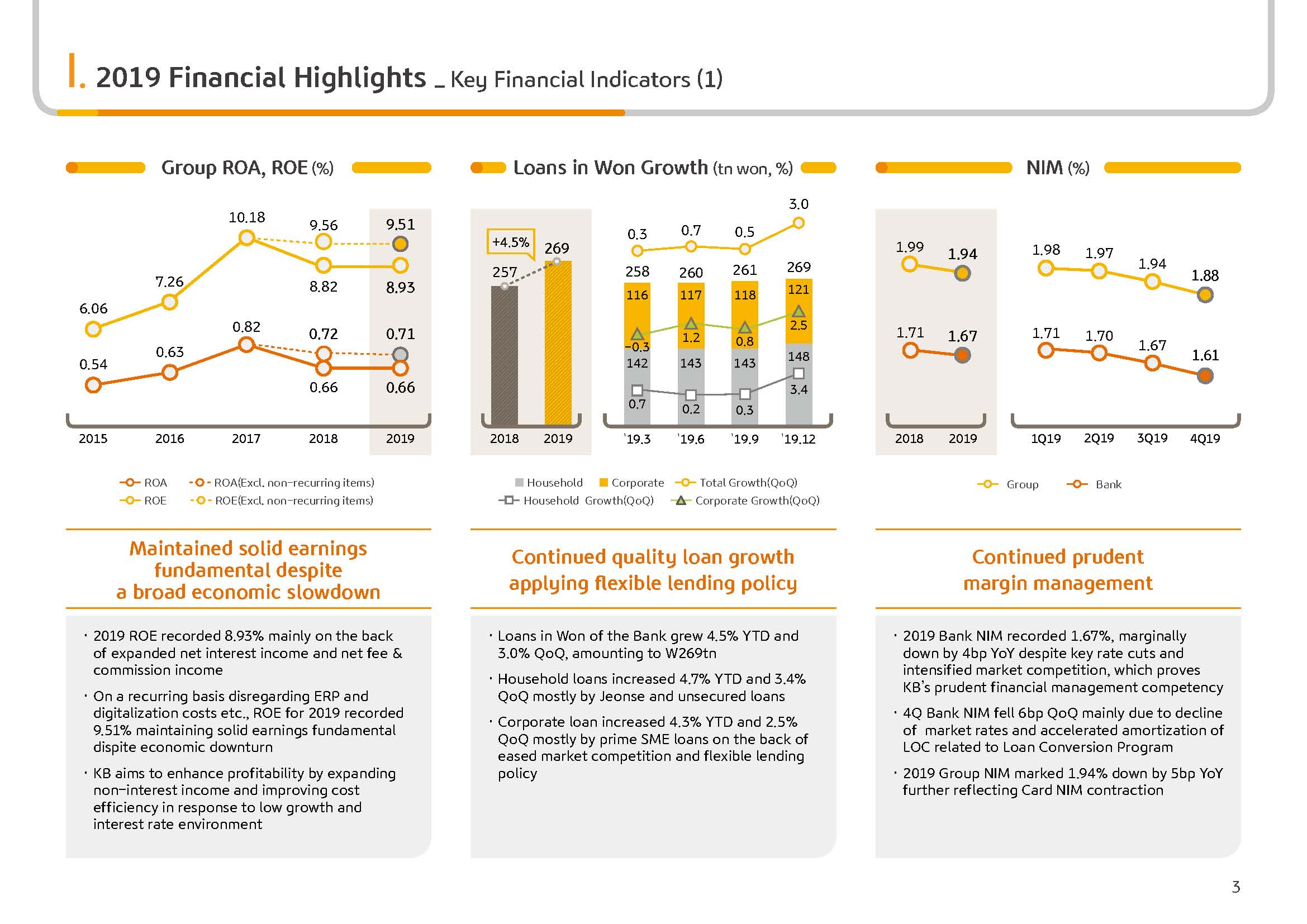

Now let me introduce our key financial highlights on the next slide. 2019 group ROE was 8.93%, up slightly year-on-year. Normalized ROE, taking out any particular one-off, was 9.51%, representing, in spite broad concerns over deteriorating profitability from the economic slowdown, firm underlying fundamentals for the group.

Next, on to growth of bank loans in won. As of the end of 2019, bank loans in won posted KRW 269 trillion, growing 4.5% YTD and 3% Q-on-Q. Household loans centered around Jeonsae and unsecured credit loans grew by 4.7% YTD and 3.4% Q-on-Q, while corporate loans, driven by high-quality SOHO, SME loans grew by 4.3% YTD and 2.5% Q-on-Q. This year, we intend to continue to carry forward quality-driven growth with utmost priority on asset soundness and profitability considering the possibility of a potential economic slowdown and developments in the real estate market. We however intend to be a bit more flexible in our lending policies compared to last year to respond to downward pressure on NIM and build a bigger basis for interest income.

Next, please look at the NIM graph on the right. The group and bank 2019 NIM posted 1.94% and 1.67%, respectively, and slightly fell year-on-year. However, despite the two base rate cuts and intensified market competition, the bank NIM was well defended in dropping by just 4 bp year-on-year, proving KB's prudent financial management competency. On the other hand, Q4 bank NIM dropped by 6 bp Q-o-Q with the market interest rate decline and amortization of LOC related to the loan conversion program.

(4p) 2019 Financial Highlights-Key Financial Indicators

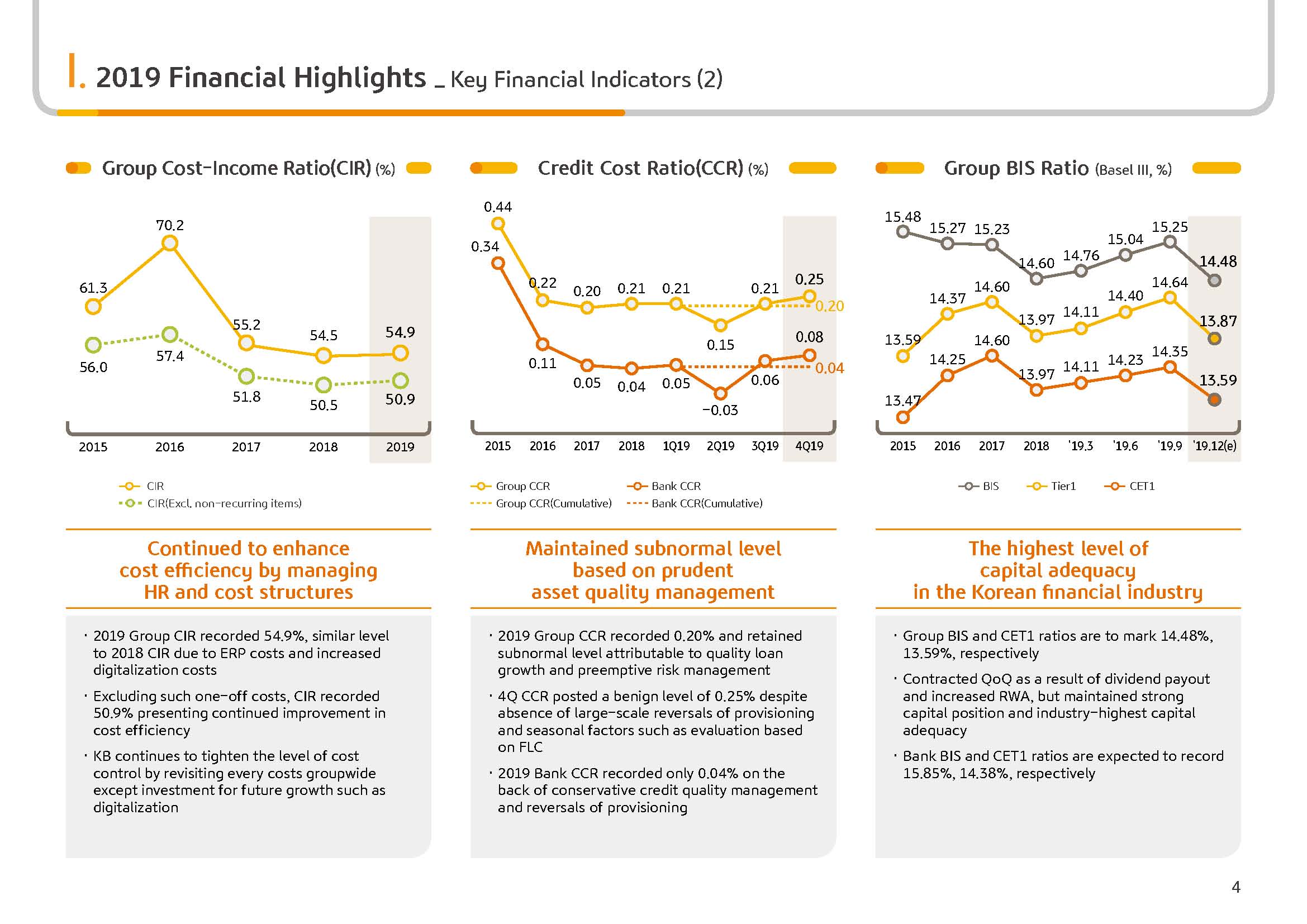

Let's go to the next page. I would first like to elaborate on our group cost income ratio. The group CIR in 2019 posted 54.9%, a similar level to the previous year with the increase of bank ERP cost and group-wide digitalization-related costs. Excluding these one-offs, CIR, on a recurring basis, recorded a 50.9% level. KB Financial Group, through solid top line growth and cost management, aims to gradually improve cost efficiency. And in particular, we aim to tighten the level of cost control by revisiting all group-wide cost from zero base, excluding investment-related costs for future growth. Although the CIR, which has been continuously improving, seems to have come to a standstill in the 50% range with the recent cost increase related to digitalization, we expect labor cost reductions to become more visible over time and expect the Group CIR to improve to a mid-40% level in the mid- to long-term.

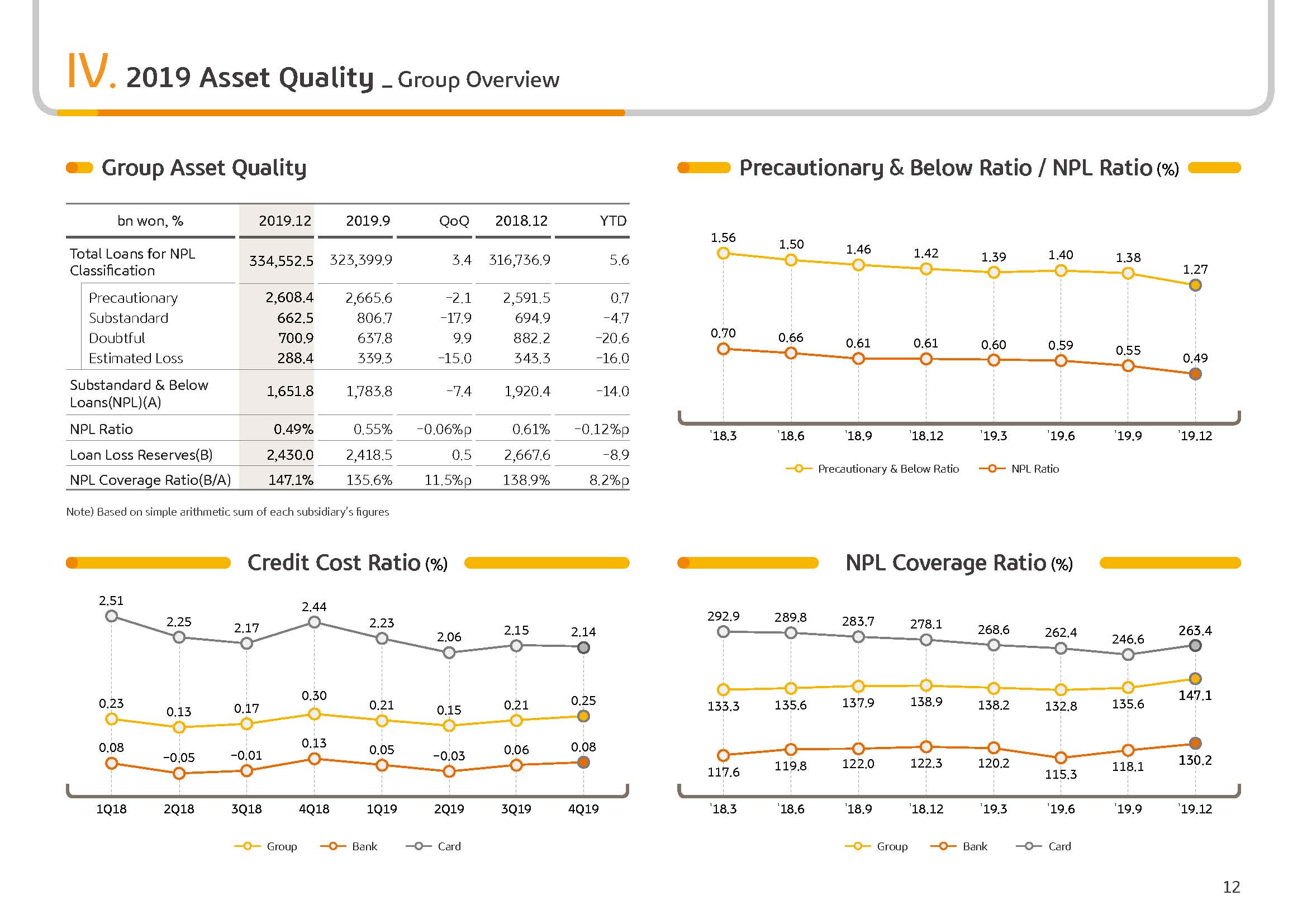

Next, I would like to elaborate on the credit cost. 2019 group credit cost posted 0.20% and, on the back of asset quality-focused loan growth and provisioning reversal, maintained a subnormal level. And the group credit cost in Q4, despite seasonal factors, including year-end FLC valuation and no sizable provisioning reversal, posted 0.25%. This year's group credit cost is expected to increase from the current level since the provisioning reversal is expected to decrease compared to the past. However, since the asset's credit quality has been greatly improved, there will not be a high possibility for rapid increase in the provisioning burden due to asset quality conversion.

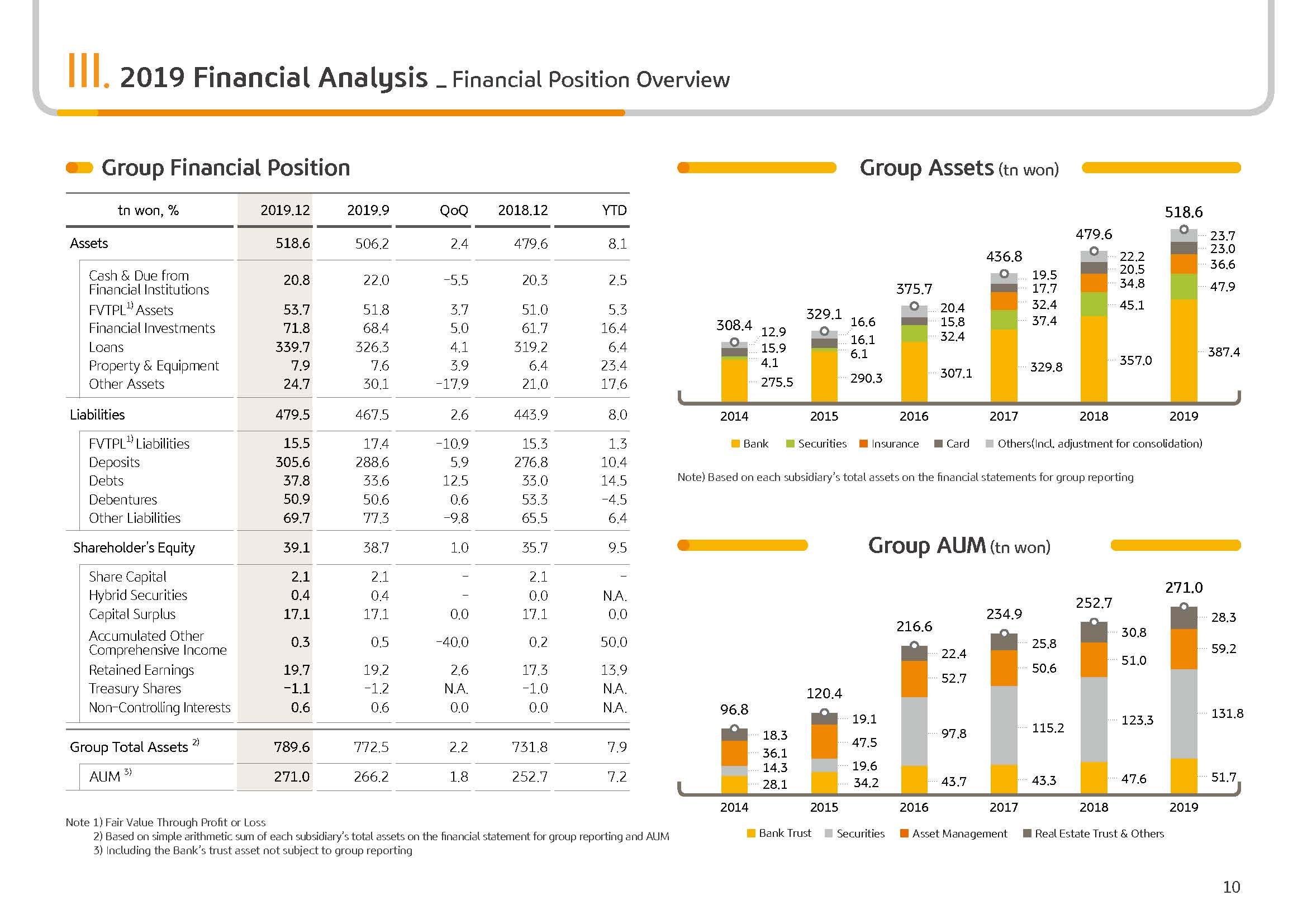

Next, I would like to elaborate on the group's capital adequacy ratio. Group's BIS ratio as of end 2019 posted 14.48%, and CET1 ratio posted 13.59%, respectively. Despite the increase in the net income, with the increase in risk-weighted assets and impact from year-end dividend, the BIS ratio decreased Q-o-Q. However, we are still meeting the best level of capital adequacy in the domestic financial sector.

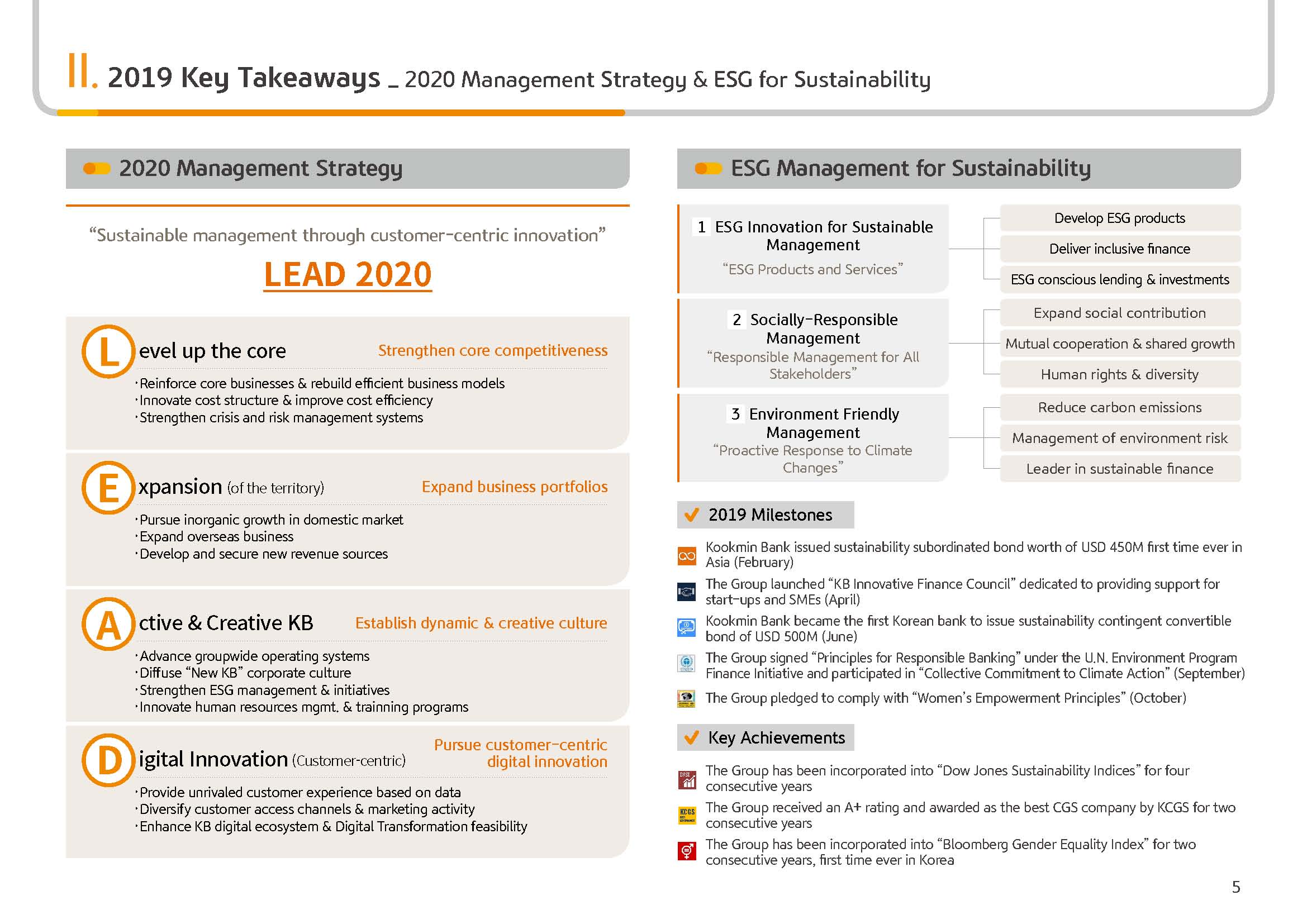

(5p) 2019 Key Takeaways-2020 Management Strategy & ESG for Sustainability

Let's go to the next page. From this page, I will cover the 2020 management strategic direction of KBFG and our ESG-based sustainable management leading strategy. KB Financial Group's 2020 management strategic direction is sustainable management through customer-centric innovation, LEAD 2020. LEAD 2020, which is the keyword of our strategic direction in 2020, is comprised of L from level of the core, E from expansion of the territory, A from active and creative KB and D from digital innovation. Level of the core means strengthening our group's core competitiveness; expansion of the territory means expanding our business portfolio; active and creative KB means establishing dynamic and creative culture; and lastly, digital innovation means our management’s strategic direction of pursuing customer-centric digital innovation.

Following the meaning of LEAD, KBFG will, this year, solidify the core businesses of our subsidiaries and, at the same time, find opportunities to improve our group's portfolio through M&As and focus on continuously expanding our global business. In addition, within the group, based on nimble and efficient operating system, we will maximize our cooperation and synergy. We will focus on our customer-centric digitalization effort so that it can lead to tangible results.

Next, I would like to cover the ESG-based sustainable management strategy of KBFG. KB Financial Group, as a leading financial company pursuing sustainable growth, plans to strengthen ESG management initiative in 2020. We will also establish an ESG system adhering to the global standard so that we can lead the way in social change and future value. To this end, KBFG has established the ESG-based sustainable management-leading strategy. First, to support the ESG innovation growth for sustainable finance, we will reflect ESG in our products and services. Second, we will internalize responsible management for interested parties, including the local community. Third, we will advance climate change strategy for the environment, so that through our ESG management activities of KBFG, we can more actively respond to the climate change issue.

Actually, the sustainable management strategies centering on KBFG's ESG was continuously executed even until now, and these efforts have led to very meaningful results and positive reviews from external institutions. For example, in February, Kookmin Bank was the first to issue $450 million of FX subordinated sustainability contingent convertible bonds in Asia. And in order for the group to more actively and realistically support the entrepreneurs, venture companies and SMEs' innovative growth, we launched the KB Innovative Finance Council. In addition, we signed Principles for Responsible Banking under the UNEP Finance Initiative in September and participated in collective commitment to climate action and actively engage in external ESG activities. As a result of these efforts, KBFG was well evaluated and reviewed by many major institutions in and out of Korea. For the first time as a Korean company, for 2 consecutive years, we were incorporated into the Bloomberg Gender-Equality Index. And for 4 consecutive years, we were incorporated into the Dow Jones Sustainability Index. We also received A+ rating and was awarded the Best CGS Company by KCGS for 2 consecutive years for our superior corporate governance. Going forward, KBFG, through expansion of ESG-based management system, will do our best to solidify our status as a role model financial group leading sustainable management.

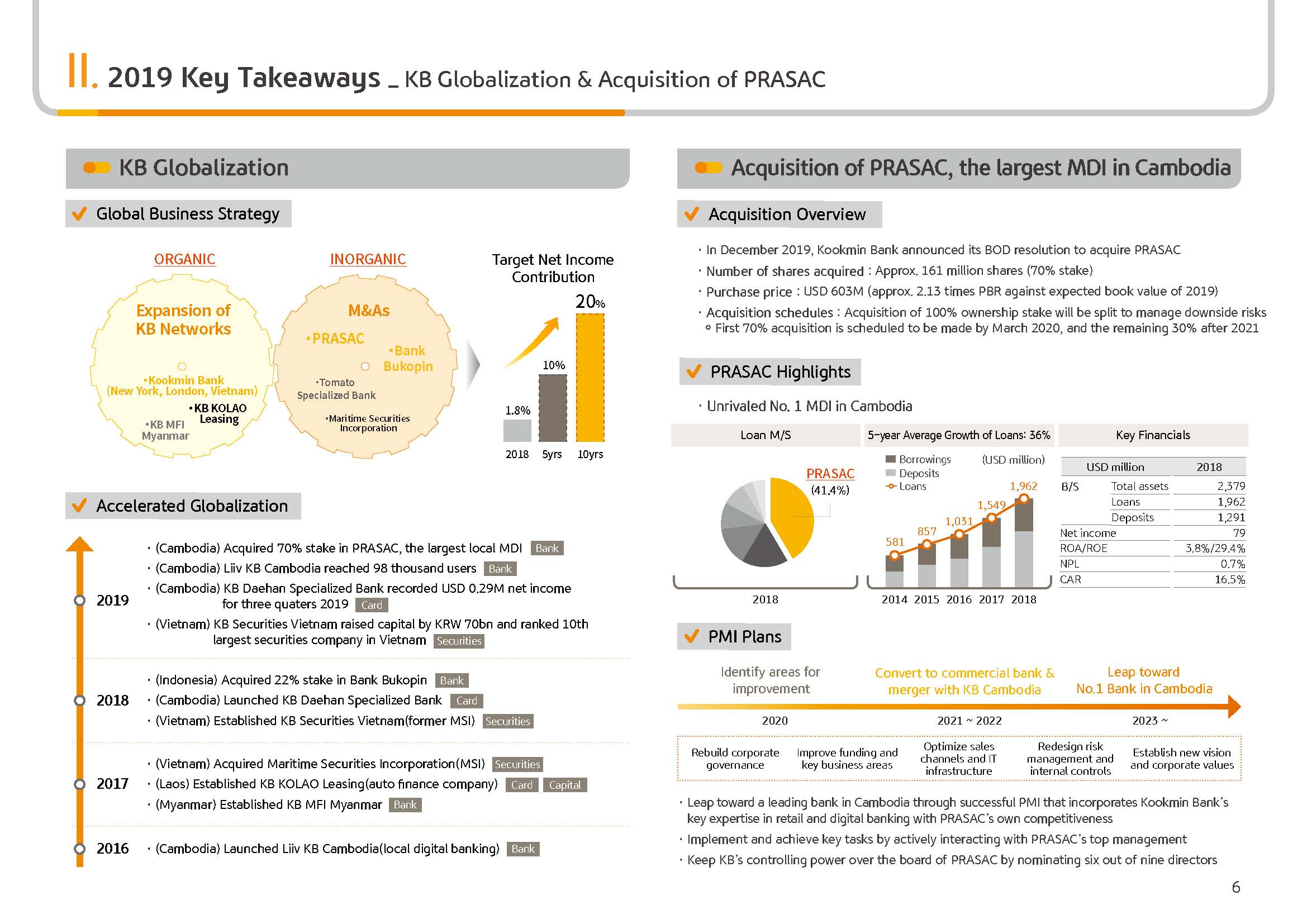

(6p) 2019 Key Takeaways-KB Globalization & Acquisition of PRASAC

From the next page, I would like to cover KB Group's globalization and PRASAC share stake acquisition. KBFG believes that in order to overcome the group limitation of the domestic market and to expand the sustainable growth engine, we need to enter into overseas markets. This is essential, and we are accelerating globalization of our group. We are focusing on entering into Southeast Asian regions, including Vietnam, Indonesia and Cambodia that have high economic growth rates and where relative early market dominance is possible. Through organic growth by expanding the existing network and expansion of working scope and through inorganic growth by acquiring local companies, we aim to expand the ratio of net income in the group, which was below 2% in 2018 and expand it to around a 20% level in the mid to long term. In particular, looking at the recent major results related to globalization, within the Cambodian market, Liiv KB Cambodia, which is the KB digital banking brand, attracted more than 100,000 members within 3 years of launching. In the case of KB Daehan Specialized Bank, a Cambodian specialized credit finance company, which was established in September of 2018, posted a profit within 10 months after launching. In addition, KB Securities Vietnam increased capital by around KRW 70 billion last year and became a top-ten securities company in Vietnam. As briefly aforementioned, in December, Kookmin Bank decided to acquire 70% of PRASAC's stock, the biggest microfinance financial institution in Cambodia. As of 2018, existing PRASAC Cambodia MDI loan market share reached an overwhelming level of 41.4%, and the recent 5 years of average loan growth rate reached 36%. 2018 ROE posted 29.4%, and NPL ratio posted 0.7%, showing industry's highest level of profitability and asset quality. Going forward, while maintaining the core competitiveness of PRASAC, we will relocate retail and digital sector capability and designate 6 out of 9 PRASAC BOD directors and keep our management controlling power. Under strict PMI management, we wish to acquire 30% of PRASAC's remaining shares and convert it to a commercial bank after 2021 so that we can go forward as a leading bank in Cambodia.

Please refer to the next pages for details regarding the earnings that I have just highlighted.

With this, I will conclude KBFG's 2019 full year business results presentation. Thank you for listening.