-

3Q20 Business Results

Greetings and Summary Greetings. I am Peter Kwon, the Head of IR at KBFG. We will now begin the 2020 third quarter business results presentation. I would like to express my deepest gratitude to everyone for participating in our call. We have here with us our group CFO and Senior Executive Vice President, Mr. Ki-Hwan Kim, as well as other members from our group management. We will first hear major financial highlights from our CFO and Senior Executive Vice President, Mr. Ki-Hwan Kim, and then engage in a Q&A session. I would like to invite our CFO to walk us through 2020 third quarter major financial highlights.

Good afternoon. This is Ki-Hwan Kim, CFO of KB Financial Group. Thank you for joining KBFG’s presentation on 2020 third quarter business results. Before presenting on the earnings, let me first brief you on the operational backdrop. As of the end of August, KBFG completed the consolidation of Prudential Life, Korea's top-tier insurer in terms of capital adequacy, sales capabilities and financial stability as its 13th subsidiary. With that, we have finally completed the acquisition of a life insurer, which was a long harnessed aim, gaining a meaningful market position in the life insurance industry. With the enhanced business portfolio, second to none in the financial industry, we are now able to further expand the group's potential for sustainable growth and profitability. Driven by robust earnings fundamentals following the expansion in our nonbank portfolio and preemptive and precise risk management, once again, we were able to record a quite stable earnings in the third quarter. However, with the prolonged COVID-19 pandemic, overall business environment for the financial industry is turning unfavorable.

With social distancing and restrictions on economic activities, macro outlook for the Korean economy continues to be negative. While financial support program for hard-hit SMEs and SOHOs have been extended by 6 more months, which deepened concerns over asset quality deteriorations and have once again put to test risk management capabilities of the Korean banks.

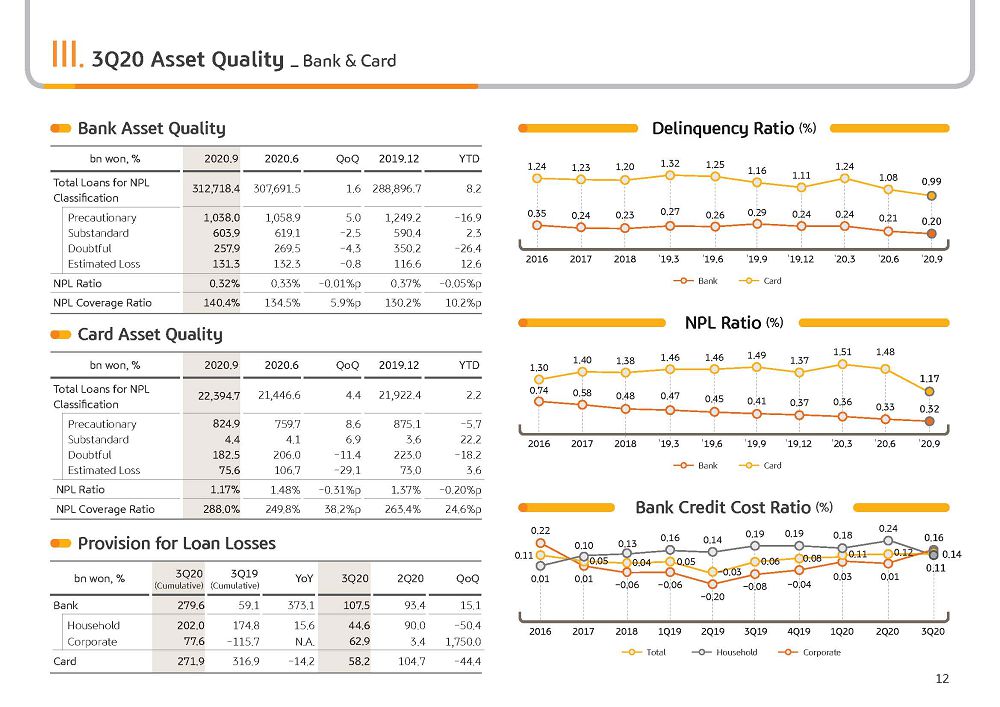

Firstly, I would like to affirm that under the crisis brought on by COVID-19, KB has kept its asset quality stable, underpinned by its rigorous risk management framework. With the extension of the financial support, i.e., moratorium on repayment, it is true that for some marginal companies there could be a carryover effect of deteriorations which would eventually lead to have impact on asset quality. However, by thoroughly analyzing basic financial information of the borrowers as well as cash flow projections taking into account impact from COVID crisis, we are reviewing debt servicing capacity and possible liquidity issues holistically as we segment risk exposures accordingly. And through such sophisticated follow-up management, we are rigorously preparing against potential risks.

Also, credit quality for the company has been improving over the years. And based on conservative forecast economic scenarios, we have made preemptive provisioning, maintaining a fundamentally robust risk management framework. As such, we expect possibility of asset quality deterioration, to the extent that it will erode our fundamentals, is quite limited.

In the meantime, COVID-19 has triggered the spread of the so-called “Untact” behavior, quickly shifting the center of gravity to digital channels when it comes to customer reaching points. KB Financial Group even before the COVID pandemic had devoted much focus to developing digital channels, by focusing on customer pain points and making improvements on convenience aspects on our platforms like “Star Banking”, “M-able” and “Liiv Mate”. And as a result, amid competitions with the big techs and other financial service platforms, our core apps are outperforming in terms of usage.

We will continue to strengthen our competitiveness in the digital channel. And by connecting it with our existing powerful off-line channel, we will lead the efforts in starting a new chapter in channel competitiveness and develop into a future-platform company with key focus on customers and the core of financial business.

(2p) 3Q20 Financial Highlights-Overview

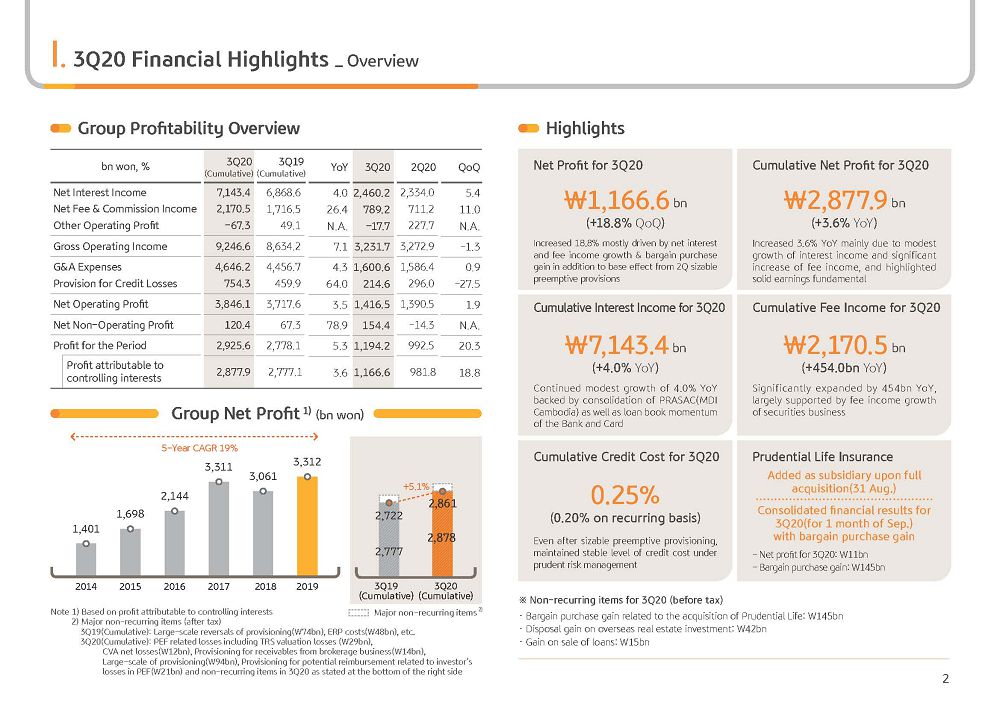

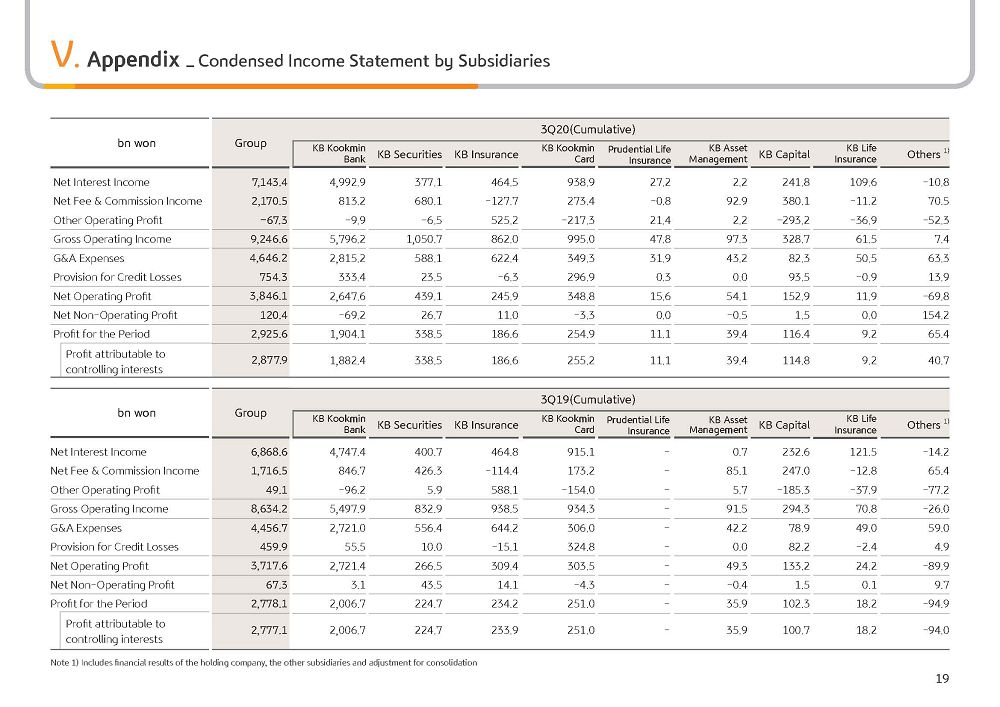

With that, I will move on to the third quarter earnings results. For your information, Q3 group performance is based on 100% consolidation of Prudential Life. So please note that in light of the acquisition date, we reflected the earnings results for a single month of September. KBFG's Q3 net profit was KRW 1,166.6 billion. On sustained growth of net interest income and net fee and commission income and a base effect of additional provisioning in Q2 as well as the negative goodwill benefit from Prudential Life, net profit was up 18.8% Q-on-Q. Excluding negative goodwill benefit of KRW 145 billion and other one-off items, recurring net profit was in the upper KRW 900 billion at a steady level, underpinned by core profit growth and asset quality management.

In terms of cumulative net profit in Q3, it came in at KRW 2,877.9 billion despite NIM being in a narrowing cycle from the rate cuts, supported by net interest income growth following solid loan growth and successful efforts to increase fee and commission income. This was a 3.6% growth year-on-year. On recurring basis, excluding the one-offs, such as last year's ERP expense and this year's preemptive and additional provisioning and negative goodwill benefit, the YoY growth was 5.1%.

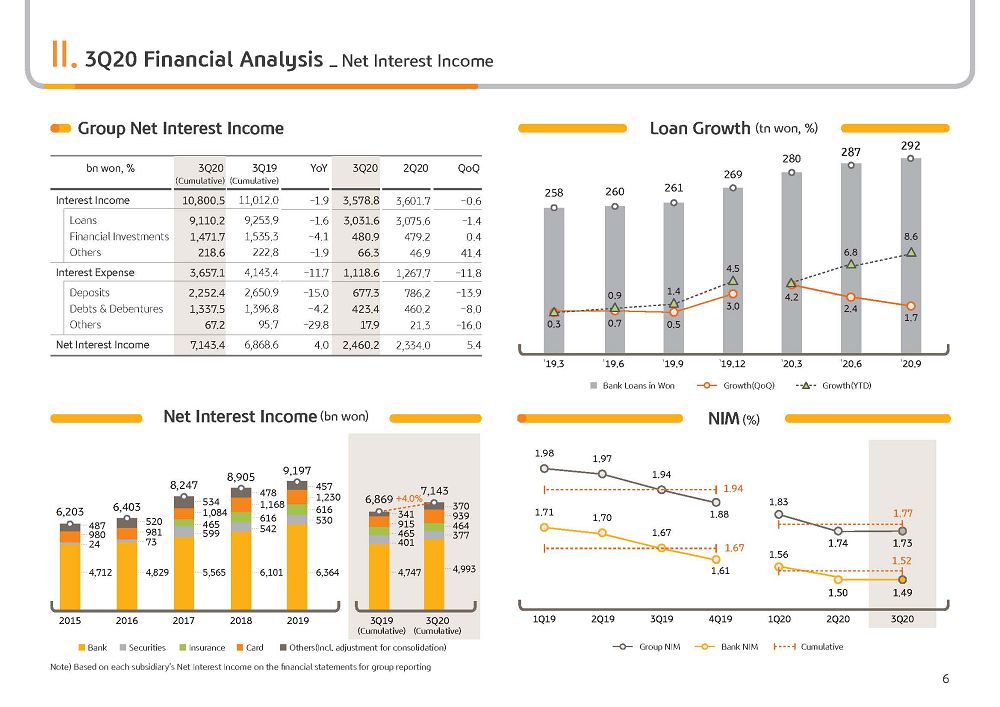

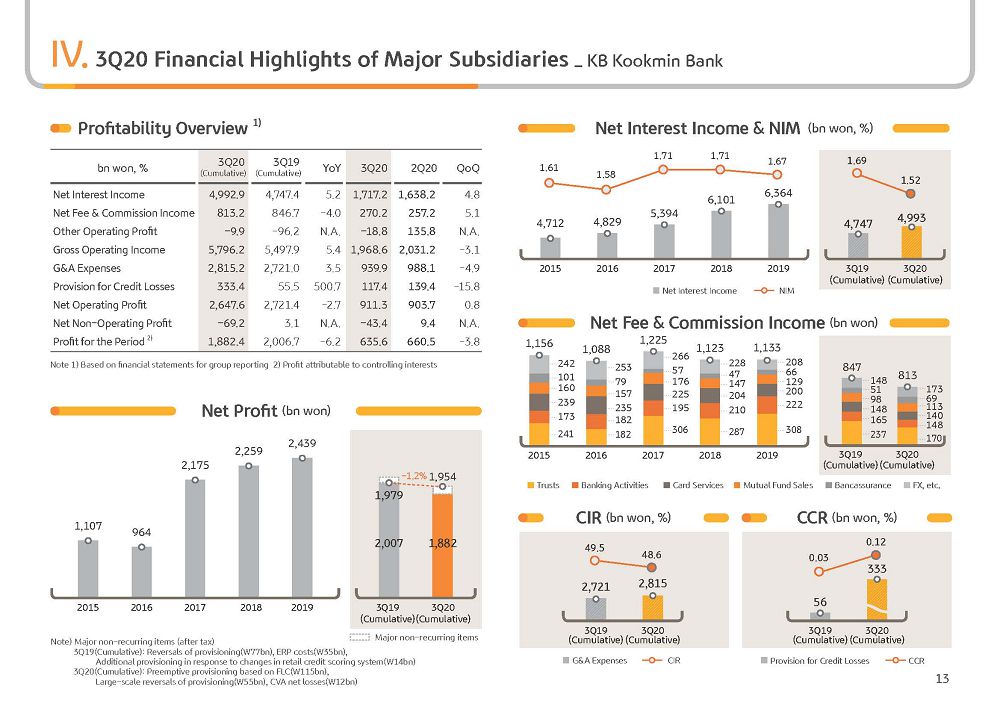

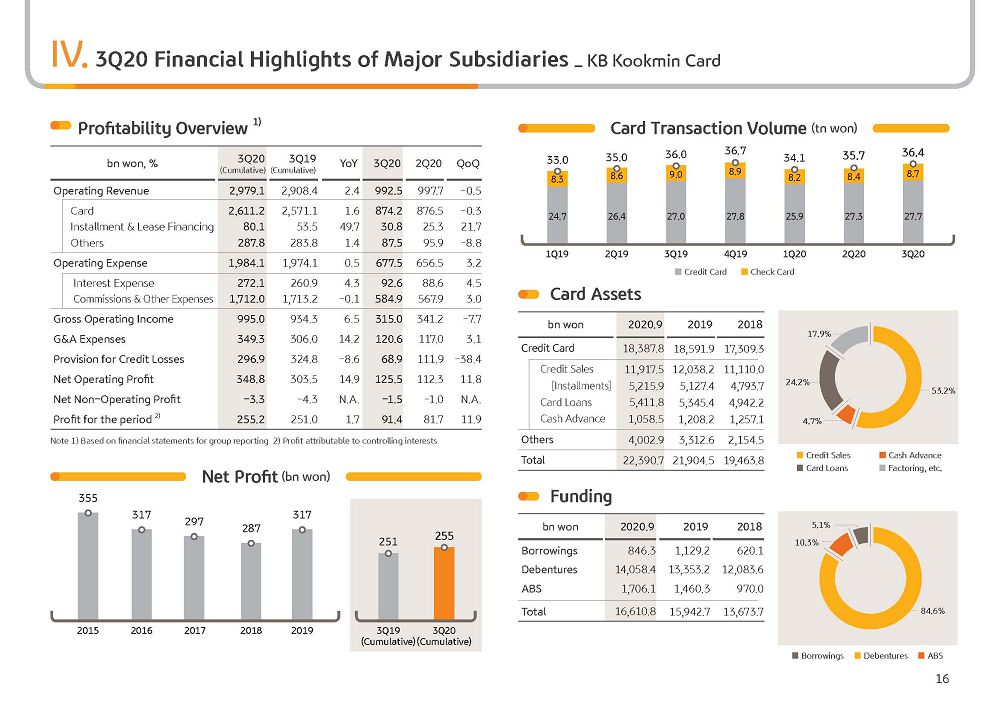

Moving on to more details by line item, Q3 cumulative net interest income was KRW 7,143.4 billion, driven by loan growth from the bank and KB Card as well as consolidation effects from PRASAC which was acquired in April. Q3 cumulative net interest income recorded a sustained growth of 4% year-on-year.

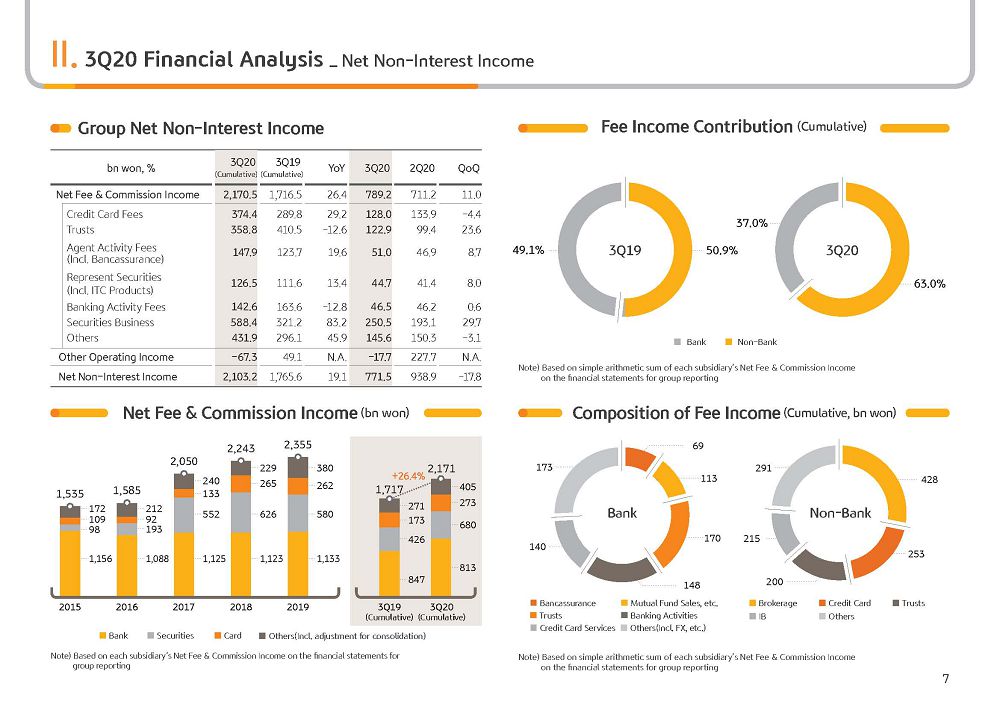

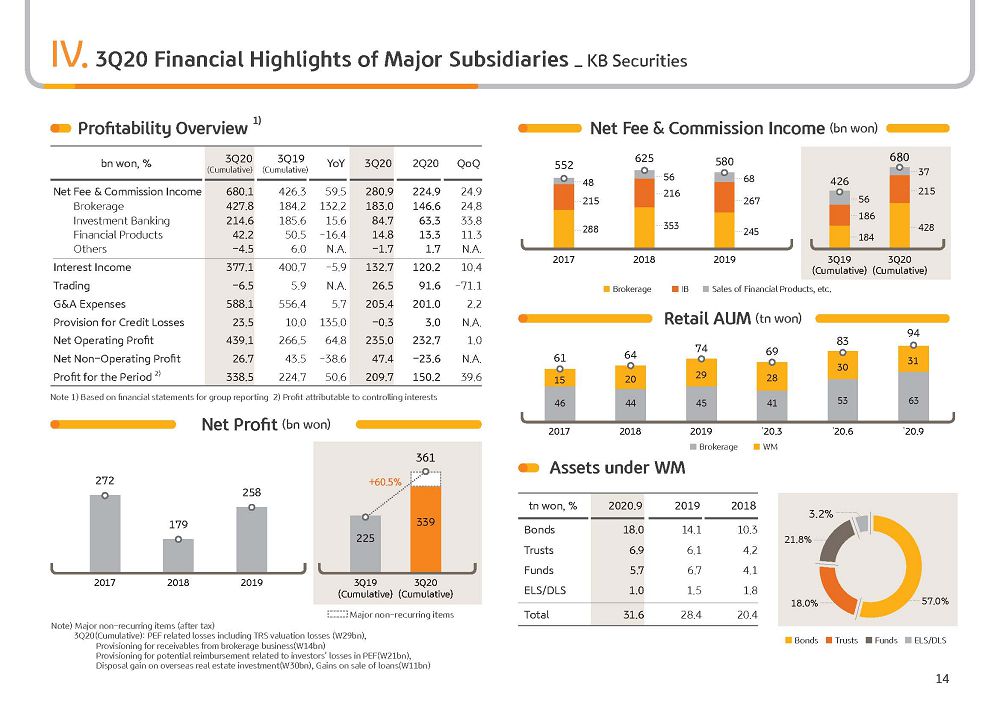

Q3 cumulative net fee and commission income was KRW 2,170.5 billion. Notwithstanding difficulties, i.e., economic recession and curtailed financial product sales, driven by growth in brokerage and IB businesses, there was a sharp increase in fee income from the securities business, pushing up the income by KRW 454 billion on year. Also, Q3 net fee and commission income reported KRW 789.2 billion, posting a growth of 11% on quarter. This was largely supported by improvement in trust fees in addition to increase in fee income from the securities business, due to increase in sales and ELS repayment after having been largely subdued in the first half due to regulatory restrictions on sales, etc.

Next, Q3 other operating income posted a loss of KRW 17.7 billion, which is a steep decline Q-on-Q. This is mainly due to the base effect of Q2, where financial market recovery has significantly pushed up gains from marketable securities and derivatives. And with August forming the trough, market rates started to rise, somewhat compressing valuation gains from bonds.

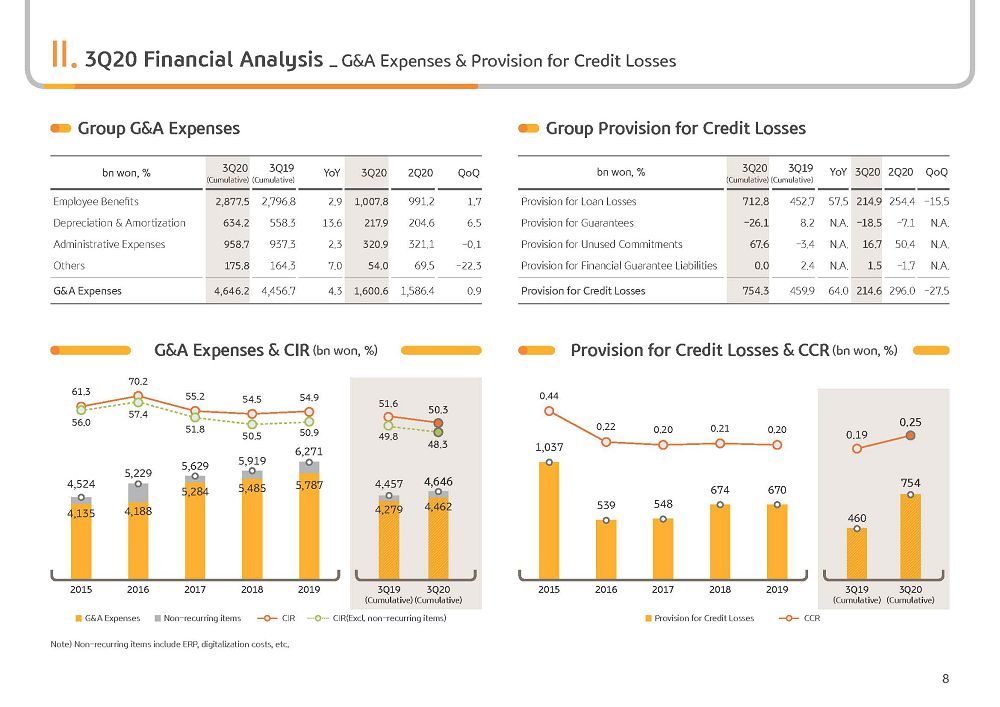

Next is on group's G&A expense. Q3 G&A expense was KRW 1,600.6 billion, a marginal increase Q-on-Q on the consolidation effect from Prudential Life. On a cumulative basis, it reported KRW 4,646.2 billion, which is up 4.3% year-on-year. Although it looks to be a sizable increase, taking PRASAC and Prudential Life impact aside, it is a 2.3% increase year-on-year basis.

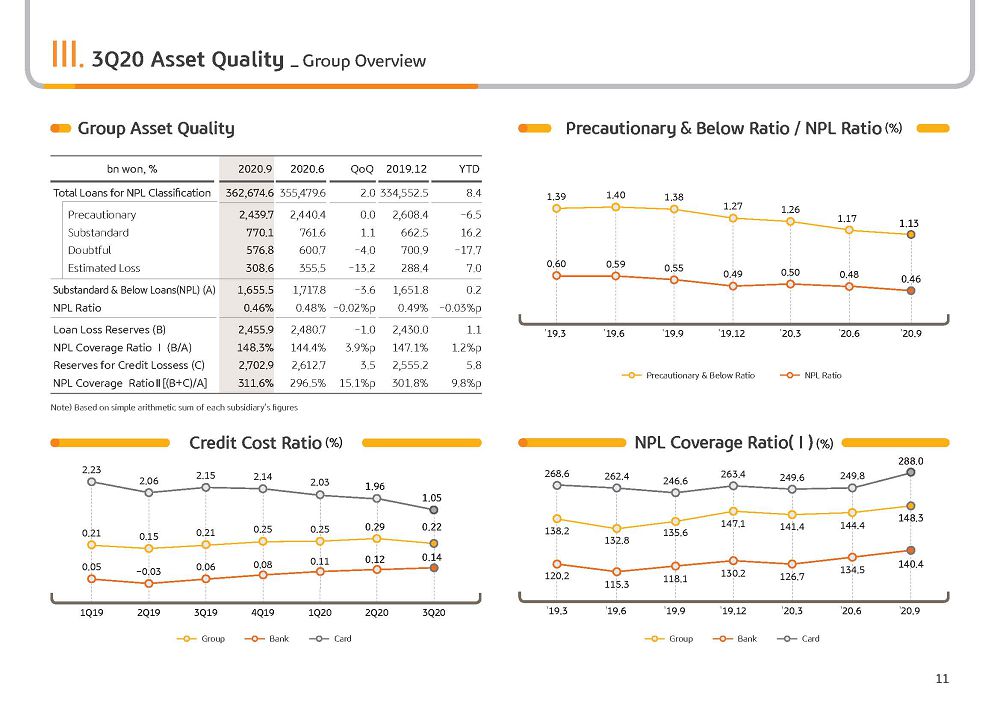

Q3 PCL, provision for credit loss, was KRW 214.6 billion, with additional provisioning impact in the second quarter removed, there was around 27.5% decline Q-on-Q, with quarterly credit costs reporting 0.22%. As such, costs are being well managed. Cumulative group PCL as of the third quarter increased significantly year-on-year on massive additional provisioning in Q2. However, credit cost continues to be at a low, stable range at 0.25%.

(3p) 3Q20 Financial Highlights-Key Financial Indicators

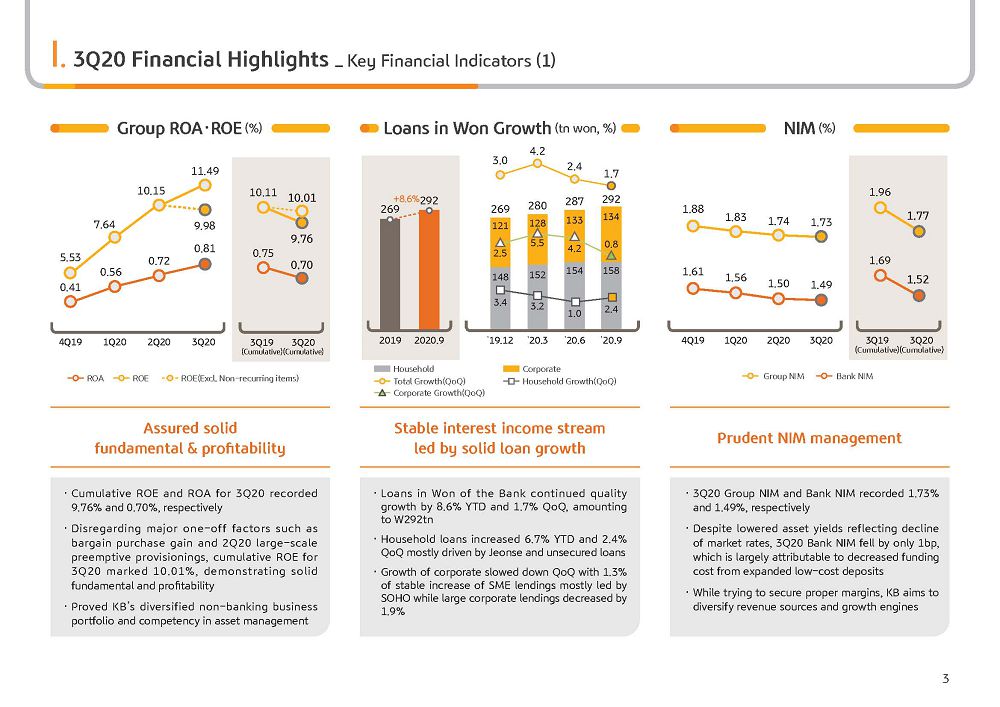

Next is on key financial metrics. 2020 Q3 cumulative group ROE and ROA respectively posted 9.76% and 0.70% and is maintaining sound fundamentals and profitability despite concerns over economic downturn. The recurring ROE, taking into account major one-offs, posted 10.01% on the back of group's core profit growth and conservative asset quality management.

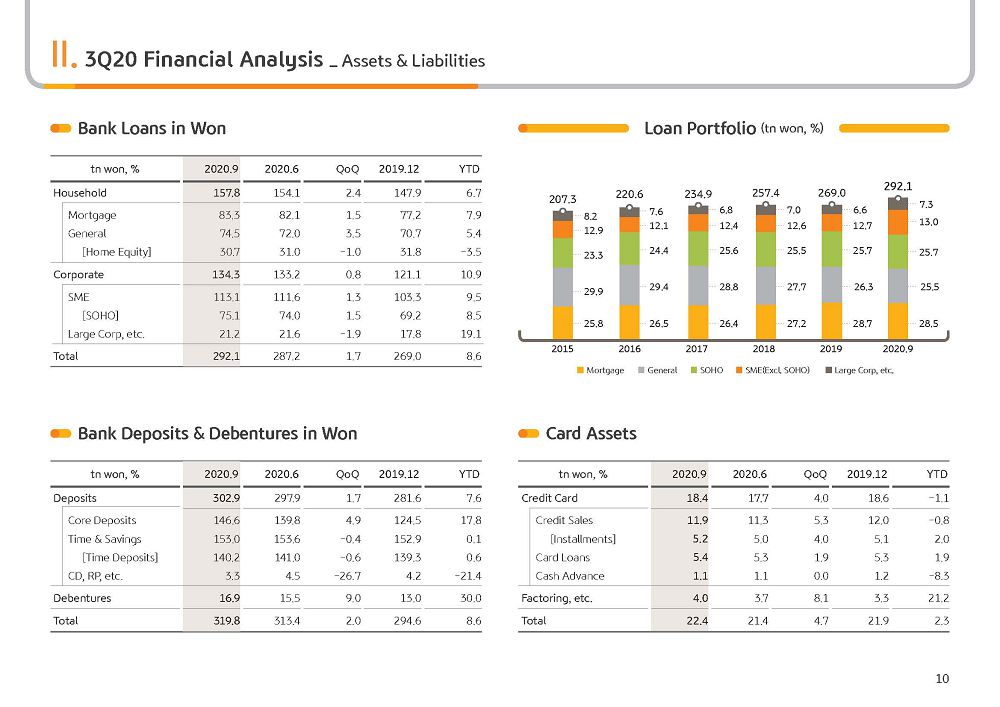

I would now like to cover the bank's loan growth in won. As of late September 2020, bank's loans in won posted KRW 292 trillion, an 8.6% growth YTD. In Q3, the focus was on quality growth centered on profitability and asset quality and grew 1.7% since the end of June. In the case of household loans, with the solid growth of Jeonse loans and prime unsecured loans, it grew 2.4% since the end of June. In the case of corporate loans, large corporate loans decreased 1.9%. On the other hand, SME loans grew stably by 1.3%, centered on SOHOs. And as a result of conservative loan policy, corporate loans grew 0.8% since the end of June.

Next is the NIM. Q3 group and bank NIM each recorded 1.73% and 1.49%, respectively. And although there was a contraction in asset yields following the interest rate cut, through efforts to increase low-cost deposits and through overall reduction in funding costs, we were able to guard the NIM, so that they both only went down 1 bp Q-o-Q. Going forward, KB, based on outstanding sales capability, will focus on expanding low-cost deposits and through a more precise and sophisticated loan pricing system, we will improve profitability and do our best to safeguard the NIM as much as possible.

(4p) 3Q20 Financial Highlights-Key Financial Indicators

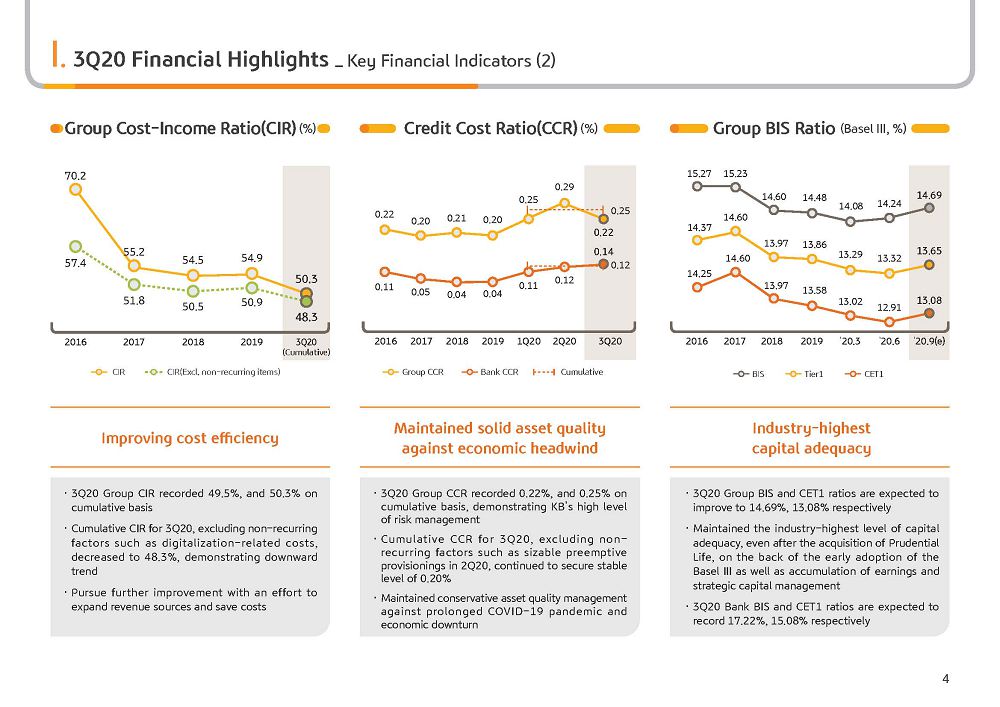

Let's go to the next page. Next, I would like to cover the group's cost-income ratio. 2020 Q3 cumulative group CIR posted 50.3%. And on a recurring level, excluding expenses, including digitalization-related costs, posted 48.3% on a recurring level. With sound top line growth and efforts to manage costs, the group's CIR is consistently showing a downward trend. With the realization of our group-wide cost cutting efforts, we forecast that it will improve to a mid-40% level in the mid- to long-term.

Next, I will cover the credit cost ratio. 2020 Q3 credit cost posted 0.22% on a quarterly basis and 0.25% on a cumulative basis, still being maintained at a stable level. In addition, excluding one-offs, including Q2 additional preemptive provisioning and sizable write-backs, the cumulative credit cost posted a 0.20% level and is maintaining a low level despite the COVID crisis and concerns over an economic downturn, proving our asset quality management capability.

With various financial support programs being prolonged for a long time now, there are some concerns over asset quality. However, we have been preemptively preparing for these possibilities. And since we have been strengthening our management of potential NPL exposure, we believe that we can stably manage asset quality going forward in the future as well.

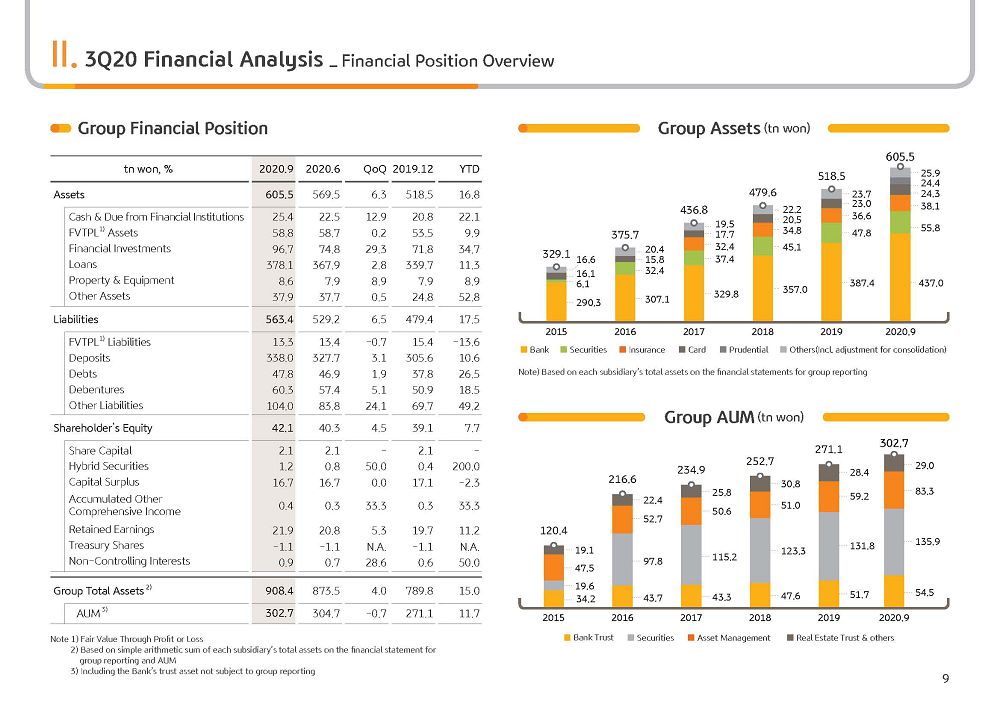

Next, I would like to cover our group's capital ratio. As of end September 2020, the group's BIS ratio posted 14.69% and CET1 ratio posted 13.08% and is still maintaining the highest level of capital adequacy in the Korean financial industry. Even after the acquisition of Prudential Life insurance, BIS ratio on the back of stronger capital through net earnings increase and hybrid bond issuance as well as the RWA reduction effect following from the early adoption of Basel III, BIS ratio rose 45 bp Q-o-Q.

For your reference, KB has applied the Basel III credit risk calculation revision plan that the Financial Services Commission decided to adopt earlier in March. With this adoption, we estimate that the group BIS ratio has been pushed up by around 130 bp.

(5p) 3Q20 Key Takeaways-Prudential Life Insurance

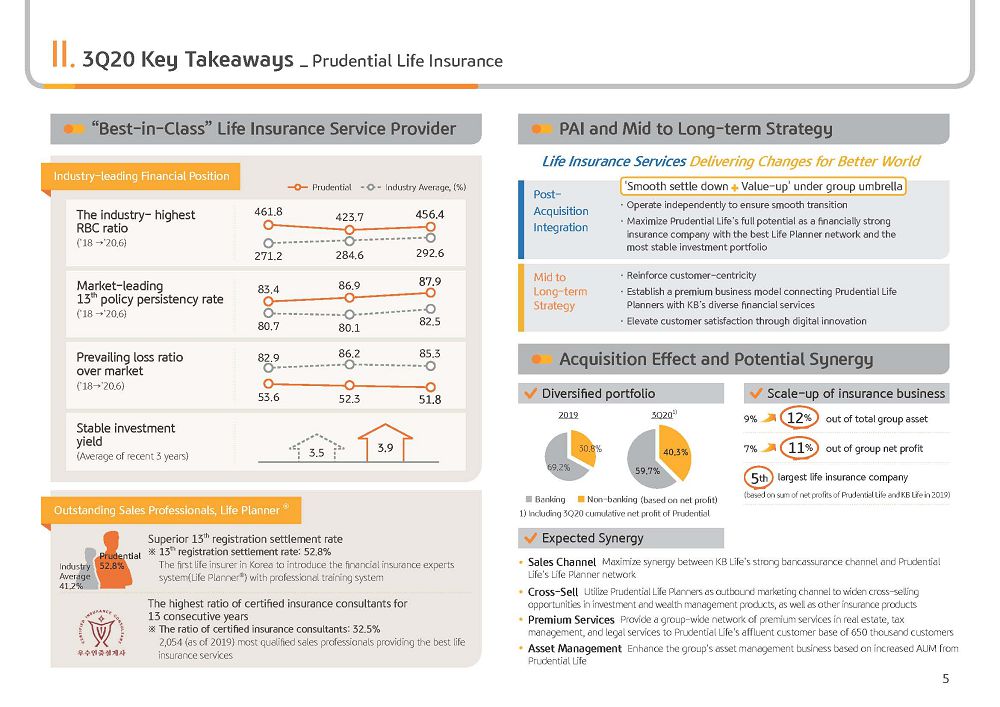

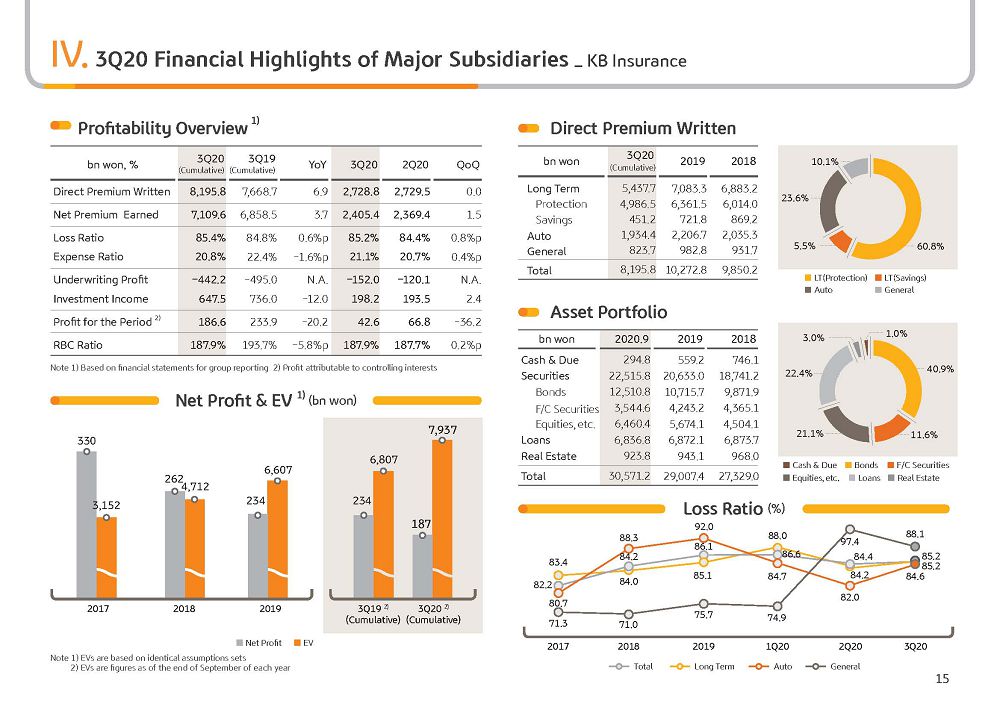

Let's now go to the next page. From Page 5, I would like to explain the management strategic direction related to Prudential Life Insurance, which became integrated as a group subsidiary from late August and the synergies we expect. Through acquiring Prudential Life, we were able to acquire a life insurance company that we had yearned for a long time. In the recent low interest environment, it is an undeniable reality that there is a bigger burden to guard life insurance company's profitability. Capital management burden is also increasing with the upcoming accounting standard and capital regulation changes. However, as we have communicated many times before, we believe that such challenges can be new opportunities for solid life insurers. And in this vein, we believe that Prudential Life can be a good partner that can develop along with our group.

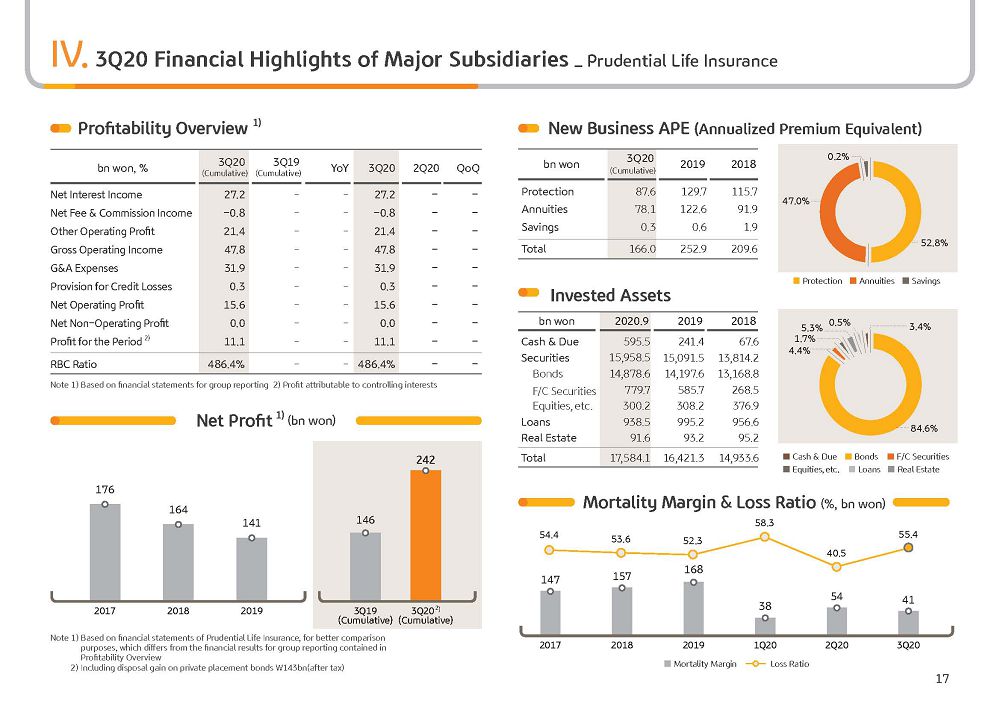

As you may be already aware, Prudential Life has the industry's highest level of financial soundness and the best sales channel. The RBC ratio as of late June this year posted 456.4% and is much higher than the industry's average, being recognized as the safest and most solid insurer from this respect. We believe that even after the adoption of IFRS 17 and K-ICS, Prudential’s solid RBC ration will be maintained. In looking at other financial indicators, the persistency ratio and loss ratio in the 13th month as of end June, each posted 87.9% and 51.8%, respectively, maintaining higher levels than the industry average.

Next, sales agents or Life Planners are recognized fully in the market as having outstanding capabilities. Prudential Life insurance is recognized by many as the “Academy of Sales Agents” because of its great strength in its systematic and professional training system that has now produced around 2,000 agents that have received this highest level of training. With this in mind, the 13th month agent retention ratio is 52.8%, which is an overwhelmingly high level compared to the industry average. The ratio of certified insurance consultants is 32.5% and has been maintaining number one in the industry for 13 consecutive years, proving that the sales agents are outstanding in many ways.

Next, to explain Prudential Life’s management strategy, in order for the smooth settlement of Prudential Life insurance into the group and to stabilize business, we will operate Prudential Life insurance independently without merging with KB Life Insurance for the time being, while the group will continuously support Prudential Life so that it can exert its unique competency as much as possible. In the mid- to long-term, we plan to connect Prudential Life’s outstanding Life Planners with the diverse financial services of KB Financial Group, establishing a premium sales model, and offer differentiated customer service through digital innovation.

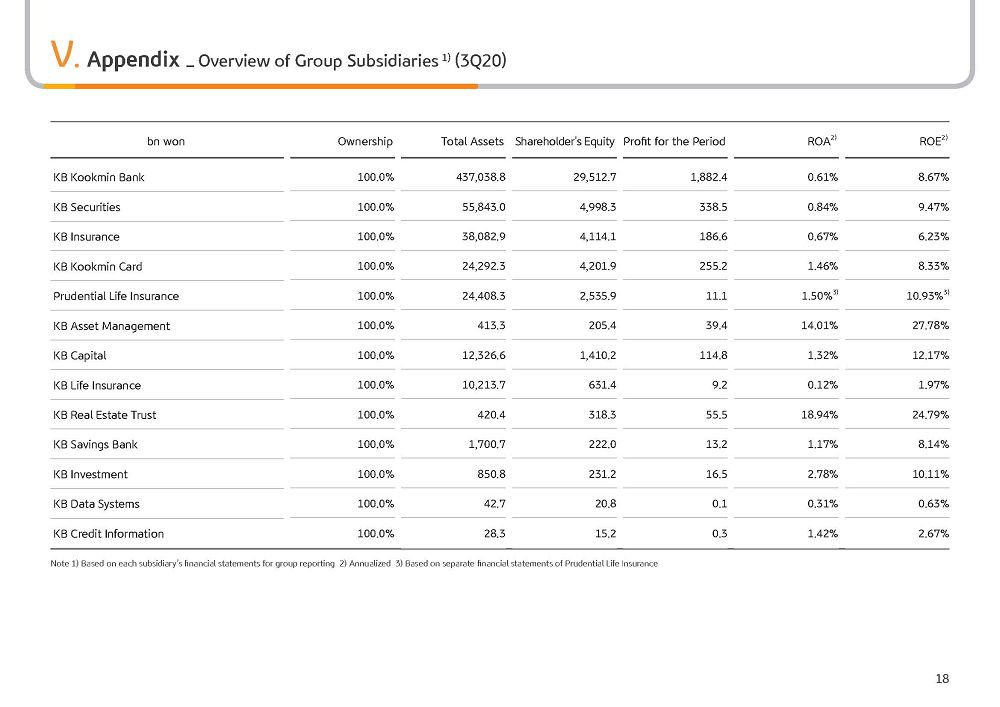

In addition, with the acquisition of Prudential Life, the group's business portfolio has been further strengthened and the position of the insurance company within the group has been heightened. The nonbanking sector contribution to the group's net profit rose from around 31% from the end of last year to around 40% based on the current portfolio. And based on the sum of net profit of Prudential Life and KB Life Insurance, our group's life insurance has become one of top five companies in the industry.

Now we are setting up strategies from the group perspective to create synergy and value in all areas, including product, channel, and organization. In mentioning a few, we will utilize the outstanding Prudential Life insurance agent organization as our group's WM outbound marketing channel to promote more cross-selling opportunities among subsidiaries. We will expand diverse financial and asset management services, including real estate, tax and legal services to Prudential Life's 650,000 customers, with a high ratio of affluent customers and create new value in the WM business.

In addition, through Prudential Life, since we have better economy of scale and bargaining power from the group, better deal sourcing will be possible, and we expect that the group's asset management competitiveness will get stronger. We are aware of some concerns in the market about cannibalization with KB Life Insurance. But since we have a strong bancassurance channel at KB Life Insurance and an outstanding Life Planner organization at Prudential, we are actually pursuing a strategy to maximize synergy at the sales channel. Through the acquisition of Prudential Life, KBFG has solid competitiveness in all areas of core business, including securities, nonlife insurance, capital and now life insurance, and we will leap forward once again as a leading financial group.

Please refer to the following pages regarding the details of the earnings that I have mentioned so far.

With this, I will conclude 2020 Q3 earnings report by KBFG. Thank you for listening.